Emerging corporate debt: flourishing on winning fundamentals

Emerging market corporations have weathered the Covid crisis remarkably well. Which means they should continue to be a reliable source of yield for investors.

Written by

Alain Nsiona Defise

Co-Head of Emerging Markets - Corporate

Share this article

For all the global economic damage wrought by the Covid pandemic, emerging market corporate credit has shown remarkable resilience. Not only has it ended 2020 with a gain of 7.1 per cent, with emerging market high yield corporate bonds generating a 6.6 per cent return, but its fundamentals remain more attractive than those of developed corporate bonds.1

The asset class’s appeal as a reliable source of income – and as an alternative to developed market speculative grade bonds – is obvious across number of dimensions.

Safety first

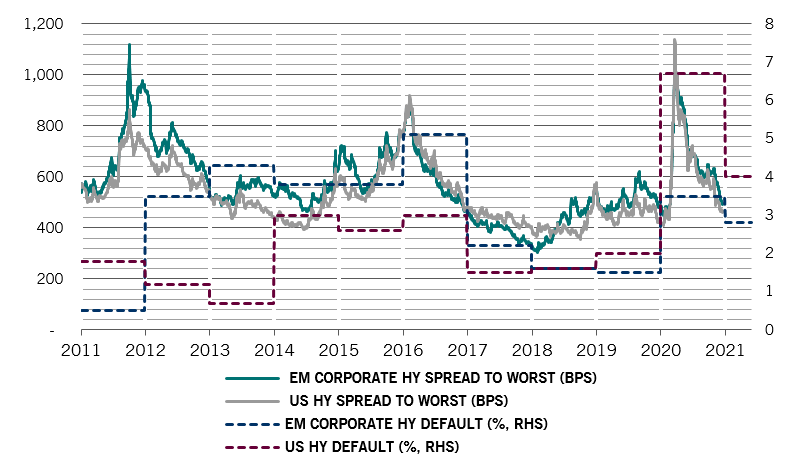

Take default rates. Despite the economic upheaval of 2020, emerging corporate bonds saw the lowest default rate among all major credit asset classes. Just 3.5 per cent of EM high yield corporate borrowers defaulted in 2020, according to JPMorgan data.

To put this into context, that rate is in line with the long-term average and just half of that of the rate registered by the US high yield bond market in 2020. It’s also well below that of the European high yield market. At the same time, recovery rates for emerging corporate debt are also vastly superior – at 42 per cent against 20 per cent for US high yield bonds for 2020, according to JP Morgan data.2

Fig. 1 - Risk and reward

Spread, basis points, vs default forecast, %, EM high yield and US high yield bonds

J.P.Morgan CEMBI Broad HY index and BAML US HY constrained index. Source: J.P.Morgan. Data from 03.01.2011 to 17.12.2020.

There are a number of reasons for this: EM high yield corporate borrowers had lower leverage than their developed counterparts entering the pandemic crisis. What is more, there have been relatively more covenant-lite high yield bonds issued in developed markets in recent years, a phenomena favouring borrowers rather than bondholders. Then there's the debt restructuring process, which is less complicated in emerging markets. In the emerging world, the process typically occurs outside the courts, taking the form of direct negotiations between borrowers and debtholders, which tends to result in more favourable outcomes for creditors.

Prudent cash management

But above all, the market's resilience comes down to emerging companies strong fundamentals. Emerging corporations enjoy a strong liquidity position, reflecting their cautious approach to cash management.

The majority entered the pandemic crisis with significant levels of cash on their balance sheets, and many have further protected their free cash flows by curtailing capital expenditures.

By contrast, developed market firms have made aggressive dividend payouts and significant share repurchases. Many are involved in increasingly frenetic merger and acquisition activity. All of which has eroded cash balances for all but a handful of tech giants and has led to a ballooning of corporate debt across leading economies.

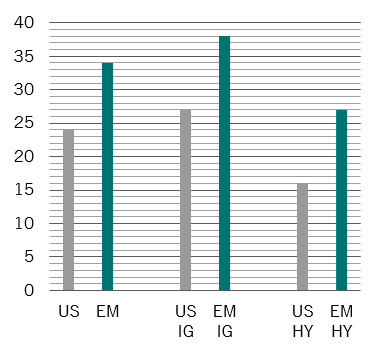

The upshot is that the average cash-to-debt ratio among emerging world corporations is now 10 percentage points higher than that of their US peers. (Fig. 2)

No-stress refinancing

Emerging market companies have also carefully managed their liabilities, buying back shorter-dated debt and issuing new, longer-maturity bonds at favourable interest rates. For instance, more than 60 per cent of newly-issued dollar high-yield bonds were used for debt re-financing in 2020, compared with 40 per cent in 2014-2017.

Fig. 2 - Emerging prudence

EM vs US corporate cash to debt levels, %

Source: Bank of America Merrill Lynch, as of 30.06.2020

Given that these issuers don’t have huge amounts of debt coming due anytime soon, there are fewer worries about their ability to service debt and, at the same time, about market oversupply. Not only do emerging corporate borrowers have ample access to dollar refinancing, but there is growing domestic demand for their debt in local currencies. Even Argentine companies managed to sell bonds to local investors at a time when they were shut out of international dollar debt markets.

The existence of state-owned or -backed banks in most of the big emerging market countries, like Brazil, India, Turkey and China, also supports demand as these banks tend to be responsible for funding strategically important domestic companies.

Structural resilience

Meanwhile, emerging market companies’ business models have been remarkably resilient in the face of Covid. To begin with, such firms are in general much less exposed to the industries hit hardest by public health measures taken in response to pandemic, such as airlines and retailers.

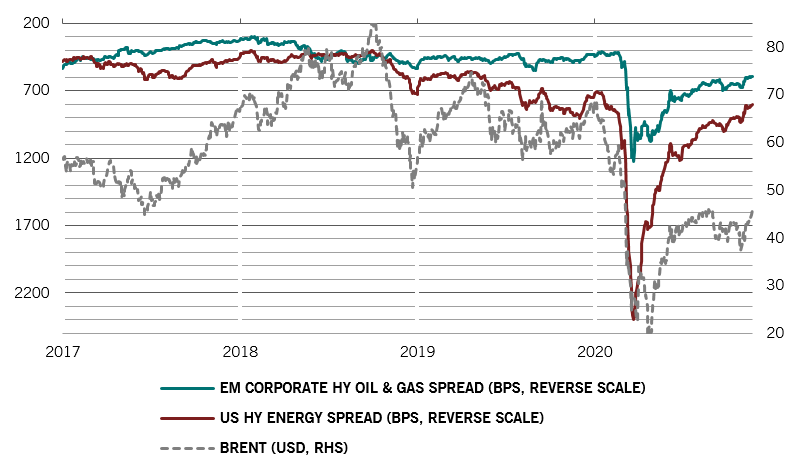

But even firms in the energy sector – which suffered considerably from declines in economic activity and the subsequent collapse of oil prices – proved much more resilient than their counterparts in the US. That’s because, by and large, emerging market energy producers are state-backed enterprises, tending to break even at lower oil prices than US energy companies issuing high yield debt. Spreads on bonds issued by emerging oil and gas companies peaked at roughly half of those on US high yield energy stocks – some 1200 basis points compared with 2400 basis points.

Fundamentally sound

Then there are the macroeconomic fundamentals. Emerging economies have generally made stronger and earlier recoveries from the pandemic-driven economic crisis. For instance, by early December all of China’s main activity indicators were above where they’d been 12 months before. Overall, emerging market industrial production was running at above fourth quarter 2019 levels. By contrast, US industrial indicators largely lagged.

And services have been picking faster in emerging economies than in the developed world, even excluding China. For instance, Brazil’s service sector is almost back to the pre-Covid levels of the first two months of 2020. That’s one of the key reasons that the developed world has been lagging: the service sector makes up 70 per cent of their economies compared to 54 per cent for emerging economies. (Fig. 3)

Fig. 3 - Less volatile hydrocarbons

Bond spreads: non-investment grade EM vs US oil and gas companies, basis points

Source: JPMorgan. Bloomberg. CEMBI Broad oil and gas high yield index, US high yield energy index; data covering period 31.12.2016-30.11.2020

All of which means the corporate default rate will continue to be below that of developed market peers throughout 2021. Crucially, this makes yields on emerging corporate bonds particularly attractive. At mid-December, investment grade emerging corporate credit was yielding 2.8 per cent, compared to 1.8 per cent and 0.2 per cent for US and European investment grade debt. At the high yield end of the spectrum, emerging world credit was yielding 5.5 per cent compared to 4.5 per cent for US bonds and 2.9 per cent for European ones.

With the spread on emerging high yield credit still wider than that of US high yield for the equivalent credit rating, this suggests scope for further narrowing of the gap, to the advantage of emerging market credit. Given the paltry yields available elsewhere in the global corporate bond market, investors would do well to consider including emerging market credit in their portfolios. Indeed, emerging market credit looks an attractive alternative to developed market credit.

Alain Nsiona Defise joined Pictet Asset Management in 2012 and is Co-Head of Emerging Markets - Corporate. Previously, Alain worked at JPMorgan in London where he was in charge of managing the Emerging Corporate franchise, worth over USD 2 billion. Prior to JPMorgan, he worked for nine years at Fortis Investments, where he started as a senior credit analyst focusing on the high yield market. He later moved to Emerging Markets Fixed Income as a senior portfolio manager building the emerging corporate business. He holds a Master's in Business Engineering from Solvay Business School, Brussels and a Diploma in Financial Analysis from the European Federation of Financial Analysts Societies (EFFAS).

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.