Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Breadth, stability and quality: Asian corporate bonds

Asia's corporate bond market has become a strategic asset class that offers decent levels of income. Crucially, it is also predominantly investment grade.

Written by

Qian Zhang

Senior Client Portfolio Manager

The negative-yielding bond was supposed to be a temporary phenomenon. But seven years after they first began to emerge across the euro zone, some USD16 trillion of global fixed income securities continue to trade at sub-zero yields. That presents investors with a problem. Income-generating assets may be in short supply but they remain essential elements of a diversified portfolio. One fix is simply to allocate more capital to lower-rated bonds. Yet that route is not be open to all. Non-investment grade bonds’ yields might be higher, but so too is their volatility.

Moreover, many investors face regulatory limits on their holdings of high yield debt. Perhaps a more practical alternative solution comes in the form of Asian corporate bonds denominated in US dollars. There are plenty of factors to commend it as a strategic holding. To begin with, there's its heft. The asset class has grown rapidly and is now home to a wide range of issuers operating across every major industry. More importantly, it is a predominantly investment grade market and also offers a substantial yield pick-up over similarly-rated issuers based in developed markets. In other words the Asian corporate bond market is both too big and too valuable to ignore.

Moreover, many investors face regulatory limits on their holdings of high yield debt. Perhaps a more practical alternative solution comes in the form of Asian corporate bonds denominated in US dollars. There are plenty of factors to commend it as a strategic holding. To begin with, there's its heft. The asset class has grown rapidly and is now home to a wide range of issuers operating across every major industry. More importantly, it is a predominantly investment grade market and also offers a substantial yield pick-up over similarly-rated issuers based in developed markets. In other words the Asian corporate bond market is both too big and too valuable to ignore.

Heft and breadth

The dollar-denominated corporate bond market is expanding fast in Asia, and is home to almost USD850 billion of tradeable securities.1 And as it gains critical mass, it is becoming more diverse, featuring issuers from a wide range of industry sectors, much like its counterparts in the developed world. A marked change in corporations’ borrowing habits has contributed to its growth.

Banks were once the primary source of funding for Asian companies. But that proved problematic. Banks borrowed short-term in foreign currency and lent long-term in domestic currency – a mismatch in maturity and currency that left domestic banking vulnerable to sudden stops in foreign financing.

Alert to that risk, Asian governments have delivered reforms to develop domestic bond markets, These efforts, which are aimed at improving market infrastructure, widening the domestic investor base and enhancing investor protection, include:

- Introducing mutual funds and individual savings accounts;

- Lifting restrictions to foreign investors;

- Introducing asset-backed securities and mark-to-market system;

- Establishing inter-dealer brokers to act as intermediaries;

- Removing the limit on corporate bond issuance amounts;

- Creating new exchanges and improving corporate governance and disclosure.

Such measures are paying off. Bonds are becoming a more popular source of funding for Asia-based firms. The total amount raised in corporate bonds per year rose to 4.5 per cent of GDP in 2008-2017 from 1.6 per cent in 1990-98, while the share of corporate bonds in total corporate financing has increased at least ten-fold in the 10 years to 2015 from less than 1 per cent.2

The expansion looks set to continue. Asian businesses’ need for capital will grow in the coming years as the region’s economies forge closer trade links and invest heavily to build capabilities in technology, manufacturing, agriculture and natural resources.

Corporate bonds, then, are sure to play a more prominent role in the region’s economic development. The asset class does not just offer an attractive avenue for local companies to access funds; it can also act as a crucial backstop by substituting bank loans or equity financing should domestic lending conditions tighten.

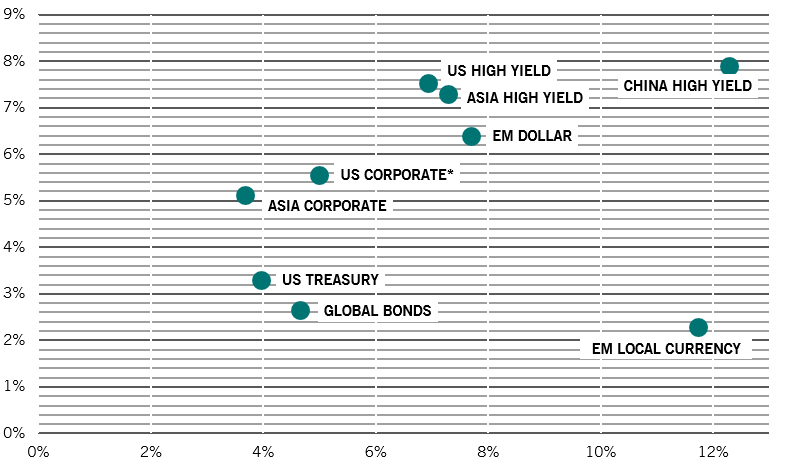

Fig. 1 - Higher quality, higher yield

Yield to maturity, %

Fundamentals to the fore

But greater market breadth and depth aren’t the asset class’s only attractions for non-domestic investors. Its fundamentals demand closer attention, too.

To begin with, and despite its expansion, the quality of issuers has remained high. The asset class is dominated by top-ranked investment grade bonds, which make up a hefty 70 per cent of the market. Then there’s yield. At a time when more than USD16 trillion of bonds globally offer negative yields, Asian investment grade credit stands out for the substantial yield pick-up it offers over benchmark US government bonds. It also trades at a higher yield than US speculative grade debt. (see Fig. 1).

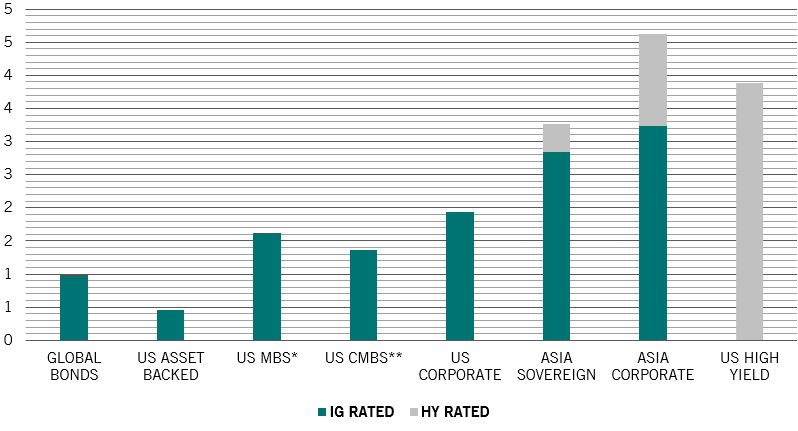

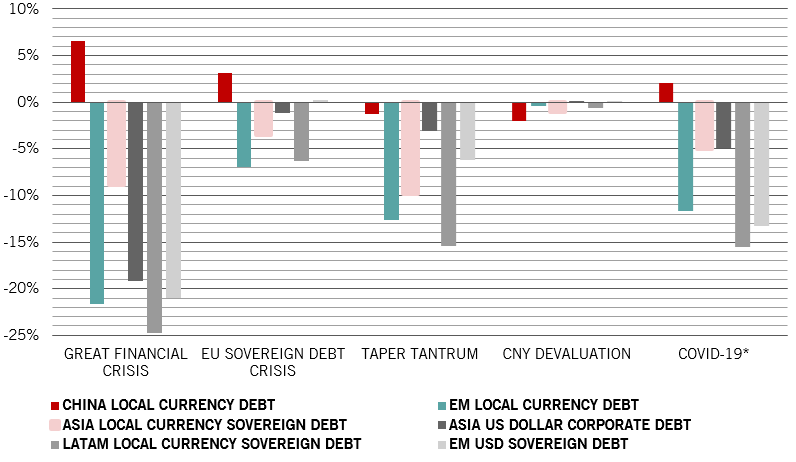

Fig. 2 - A line of defence: Asia corporate bonds hold up well during bouts of turbulence

Peak to trough loss, by asset class, %

Fig. 3 - Solid return without the volatility

Annualised return and volatility, by bond asset class, %

There are good reasons to believe this will continue to be the case.

Prudent cash management. Asian companies tend to have nearly twice as much cash on their balance sheets and lower net leverage compared with their developed market peers. Investment grade Asian corporate issuers have, according to JP Morgan, a net leverage ratio of 1.4 while their cash holdings are equal to 42 per cent of their total borrowings. That compares favourably to US investment grade issuers, for which the respective figures are 2.4 and 24 per cent.

Low exposure to commodities. Asia’s bond market is not especially sensitive to commodity prices, which can be extremely volatile. This is particularly true for corporate debt, which has a lower proportion of issuers from the oil, gas, metals and mining industries than the bond markets of other regions but increasingly features companies from dynamic sectors such as renewables and telecoms.3

Home bias. The Asian corporate bond market benefits from a large and stable domestic investor base, which represent around 80 per cent of all investors. This group of primarily asset managers and institutional investors tends to have a longer time horizon and a greater tolerance for currency fluctuations, which helps reduce the overall volatility of the asset class. For example, in Korea, the combined holdings of pension funds and insurance companies account for nearly half of the corporate bond market.4

Income at an affordable price

A market that is becoming deeper and more liquid, Asian credit should represent an attractive opportunity for international investors keen to diversity their fixed income portfolio and participate in a long-term transformation of Asia’s economies.

more on emerging fixed income

Rise of emerging Asia: promising investment opportunities in the next five years

Which EM Asia asset classes do we expect to do well in the future? Pictet Asset Management Strategy Unit presents return forecasts for emerging Asia’s stocks and bonds vs. the rest of the world. Find out how investors can capture investment opportunities in the region.

July 2021

Investing in Chinese bonds

An emerging asset class of global significance

February 2021

New Asian century: post-pandemic opportunity

Why emerging Asian assets will grab a greater share of global investors' portfolios.

February 2021

Investing in Chinese bonds

An emerging asset class of global significance

February 2021

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.