Asset allocation: equities ripe for a rally

The Covid-19 vaccines allow us to look beyond the pandemic and focus on the strengthening economy, which remains supported by substantial flows of emergency fiscal spending.

This benevolent macroeconomic backdrop is a boost to corporate profits, and should offset any decline in stocks’ price-earnings multiples caused by a wind-down of monetary stimulus.

At the same time, the risk of a policy mistake or a fresh jump in bond yields such as happened in 2013 when the US Federal Reserve decided to taper its asset purchases is low over the next six months. So although equity valuations and investor sentiment are both unusually high, the prospects of a near-term correction look limited. For these reasons, we have decided to upgrade equities to overweight from neutral and reduce cash to underweight.

Our business cycle indicators are positive for riskier assets. We expect 2021 economic growth to beat current market expectations – our forecast is for global real GDP to expand by 5.8 per cent this year against a consensus of 5.1 per cent. China is firing on all cylinders, with nearly all of the country's key economic activity indicators running at well above the levels seen 12 months ago. This, in turn, is helping support the rest of Asia.

We also expect the US and Japan to fare well: fiscal support will be significant while the pandemic’s winter wave will, we believe, have only a mild impact on both economies. Business investment in the US should also rise as companies, buoyed by signs of rising demand, start to deploy the cash they have amassed in recent months.

The outlook is more challenging for Europe and the UK, even if the the Brexit deal agreed at the very end of 2020 reduces some of the risks threatening the region. For now, inflation shouldn’t be a concern, given substantial unemployment and the fact that monetary policy operates with significant lags. Price pressures are more of a concern for 2022.

Liquidity remains plentiful and continues to support financial markets – the volume of monetary stimulus may be down from the summer’s unprecedented levels, but it is still around pre-pandemic peaks, according to our indicators, which measure both private sector liquidity and that provided by the five major central banks.

However, the downward trend will eventually matter for investors. We expect global liquidity supply to start contracting by the second quarter of 2021, led by Asia. This could trigger a material reduction in equities’ price-earnings multiples, much as happened during the global financial crisis.

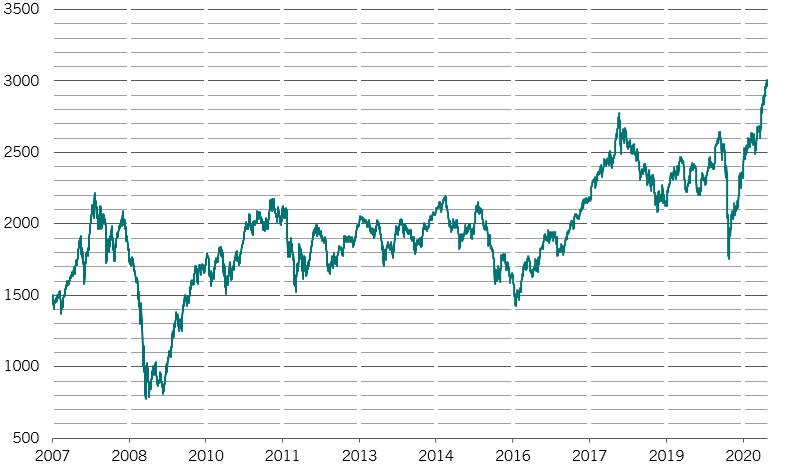

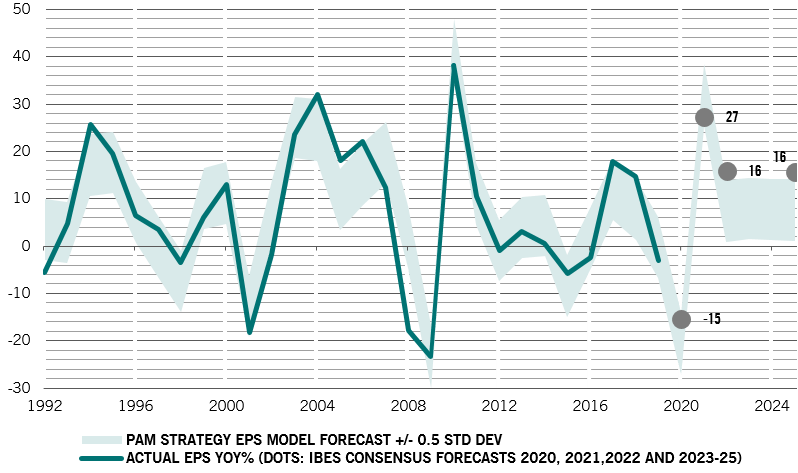

Valuations appear high in all the major asset classes. Not only has ultra-easy monetary policy driven bond yields to record lows but investors anticipate a strong economic recovery. Equities are at their most expensive since 2008 according to our models. Simply put, markets aren’t factoring in the prospect of any bad news for 2021. Global equities trade at 20 times 12-month forward earnings, while for US equities that ratio is now 23 times. Although we expect price-to-earnings ratios to contract next year, this should be offset by strong corporate earnings, which we see growing by 25 per cent in 2021.

Our technical indicators aren’t showing any reason for concern, apart, perhaps, for the corporate bond markets. Generally, our charts suggest riskier assets have further to run, seasonality is supportive, and the rally has moved beyond just the leading tech stocks. Although inflows into equities have recently been significant, some of that is down to investors making up for under-investing earlier in the year. Some sentiment indicators of investor sentiment are starting to flash red as they highlight near historic levels of bullishness, which, in the past, have foreshadowed a market sell-off.