Asset allocation: Maintaining perspective

There is no summer lull for investors this year. The global economy is powering ahead despite the resurgence of Covid-19 infections while inflationary pressures continue to build, particularly in the US. Then there’s renewed upheaval in China.

The Chinese government’s surprise ban on for-profit after-school tutoring, essentially shutting down the circa USD100 billion edu-tech sector, has raised concerns about an intensification of Beijing's regulatory crackdowns. The latest intervention comes on the heels of cybersecurity investigations of the ride hailing app DiDi and other e-commerce companies, increased scrutiny of overseas IPOs and the imposition of fines and restrictions on some of China's largest e-commerce firms.

Authorities have also moved to restrict the use of the variable interest entities (VIE) structure – holding companies based in tax haven jurisdictions and designed to allow foreign investors to invest in key sectors such as tech without giving them any operational control.

A positive reading of such developments is that they are a belated response to the breakneck growth of tech-related industries that flourished in the absence of a regulatory framework. Even though such moves would in effect add a permanent 'risk premium' to Chinese stocks and bonds, the should not fundamentally change China’s growth model or the broader investment case for the country's financial assets.

Nonetheless, a greater degree of caution seems sensible and we feel justified in taking profits in Chinese bonds, which have performed strongly year-to-date.

August 2021

More broadly, we retain a neutral allocation across equities, bonds and cash; still, we continue to favour assets that benefit from stronger economic potential, such as European stocks.

Our business cycle analysis shows that economic activity is picking up strongly across the euro zone, following a sharp deceleration over the last two quarters. Purchasing manager indices remain buoyant, especially in the service sector. Retail sales have meanwhile recovered above the pre-pandemic trend. Bank lending conditions are also easing, which augurs well for future credit growth. Overall, it would seem that European economic growth is more likely to to surpass consensus forecasts than the US, where we are starting to see some signs that its expansion is moderating. Worryingly, second quarter GDP growth came in at just 6.5 per cent on an annualised basis – some 2 percentage points below the consensus forecast.

China’s growth has clearly peaked with industrial production, retail sales and construction all coming in below their three-year average. Even so, we still expect a very respectable 10 per cent expansion in GDP for the year – some distance above the 8.5 per cent consensus forecast.

Should Beijing’s regulatory crackdowns threaten growth, however, there is some comfort to be taken from our liquidity indicators, which show that China has plenty of monetary fire power. Indeed, we already saw authorities take action in July, when the People’s Bank of China (PBOC) announced a 50 basis point cut in the reserve requirement ratio (RRR); we expect to see more action in coming months.

The US is moving in the opposite direction, with the US Federal Reserve edging into the first stages of a tightening cycle. Notably, at its latest meeting, the US central bank highlighted the improvement in economic conditions and “progress” in the labour market. However, we expect the tightening journey to be a relatively slow one, and for now US monetary policy remains the loosest of all the world’s major economies, according to our models.

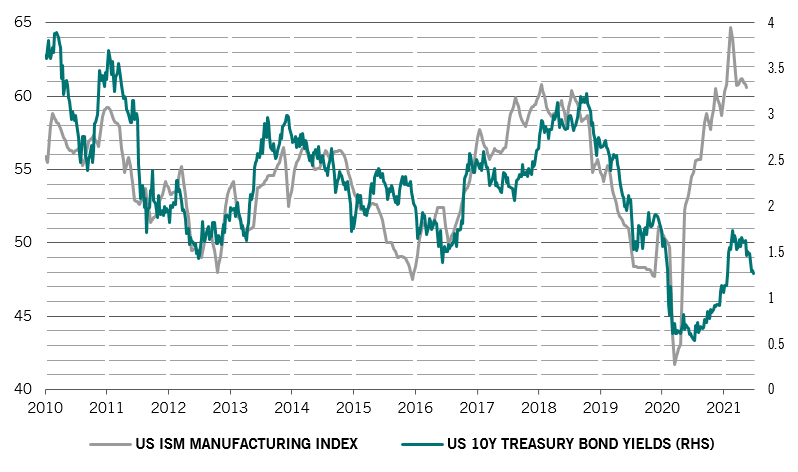

One of the clearest signals from our valuation models is that US Treasures now look expensive, particularly when compared to levels implied by the cyclical trends we monitor.

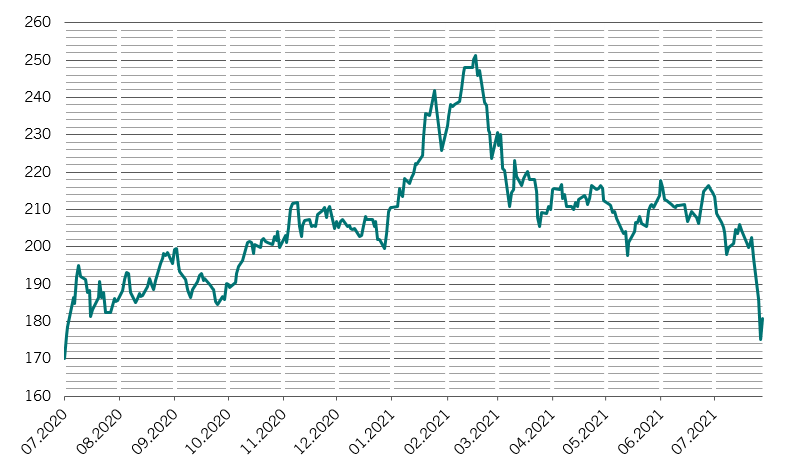

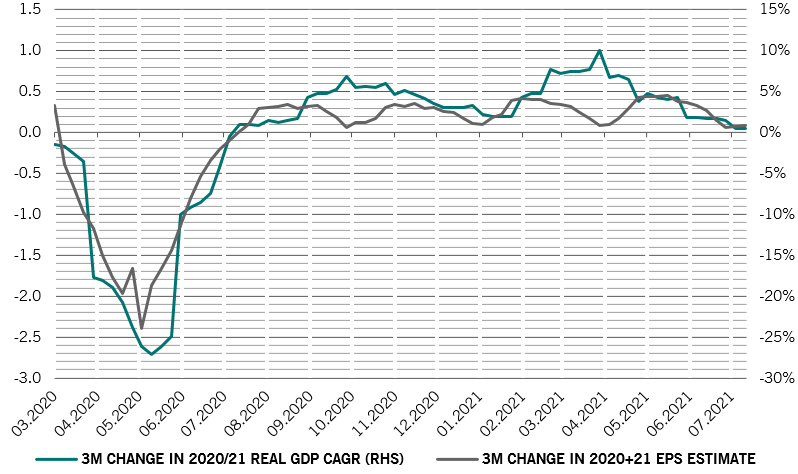

The same applies to US equities. US stocks' price-to-earnings ratio of 21.5 times based on 12 month forward earnings can only be sustained if trend growth is unchanged, profit margins are stable at high levels and bond yields stay low. So far, the recovery in US earnings has been in line with GDP (see Fig. 2), and we think further upside to this year’s corporate profit growth is unlikely in the absence of an upward revision to US GDP growth forecasts.

Source: Refinitiv, IBES, Pictet Asset Management. Data covering period 18.03.2020-28.07.2021.

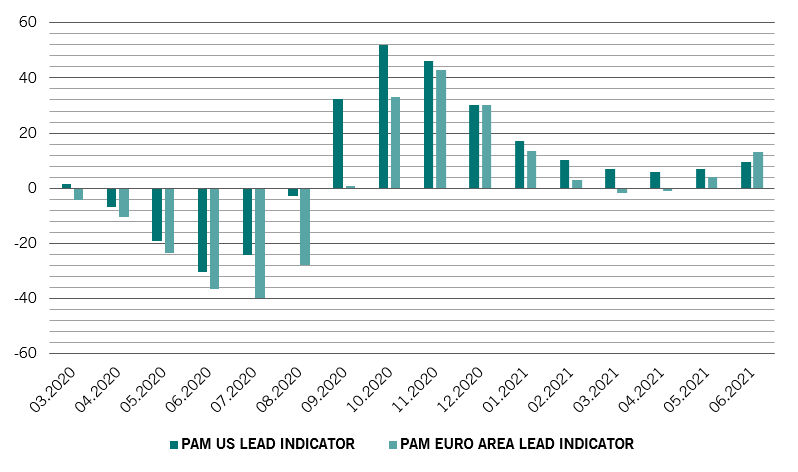

Technical indicators suggest the correlation in the returns of equities and bonds has turned negative again, improving the diversification appeal of fixed income.

Another conclusion to draw from our technical gauges is that investors appear more cautious. This is arguably reflected in the strong inflows into government bonds seen in recent weeks, as well as into equity funds that invest in quality stocks. Some USD6.7 billion flowed into tech, healthcare and consumer goods stocks in the first three weeks of July at expense of cyclical sectors, according to EPFR data. Approximately USD3.1 billion was withdrawn from financials, materials and energy stocks in the same period.