Five lessons from the pandemic

Looking back on a year many would rather forget, our chief strategist Luca Paolini discusses developments that should live long in our collective memory.

Written by

Luca Paolini

Chief Strategist

The year orthodox became history

Every global shock leaves a legacy. The Covid-19 crisis is no different. Although it will be some time before investors truly comprehend the effects of the pandemic, it is already clear that it has transformed monetary and fiscal policy for good. Central banks have abandoned monetary orthodoxy while institutions such as the Intentional Monetary Fund – once devout advocates of fiscal discipline – are urging governments to spend freely. The advice has been followed to the letter: some USD12 trillion in emergency fiscal stimulus was delivered in 2020, equal to 14 per cent of world GDP.

It is telling that even Germany, a nation whose reputation for fiscal restraint is embodied by its schwarzer null policy, has accepted that austerity no longer works. It has suspended its constitutional debt brake clause and actively supported an easing of European Union's budget constraints, paving the way for the EU’s unprecedented recovery plan (see below).

The increase in public spending has been accompanied by the return of Big Government. Even in the laissez-faire US and UK, governments have bailed out industries, offered subsidised wage schemes and provided extremely generous unemployment benefits and rent holidays. It will be difficult to reverse those policies. Indeed, it is more likely that a new Social Contract will emerge, embodying greater state intervention, more redistribution and enhanced workers’ rights.

Central banks’ metamorphosis, meanwhile, has continued apace. Radical measures to channel stimulus have coincided with a shift in policymakers' priorities. The European Central Bank and the Bank of England, for instance, are both looking at ways to incorporate climate change risks into their monetary policy frameworks. At the same time they, and many others, are also considering launching official digital currencies to allow for an even more effective transmission of monetary policy.

Central banks have more firepower than we think

The pandemic has ushered in a new era of extreme and innovative monetary easing. Defying those who claim they have run out of ammunition, the world’s central banks provided USD8.8 trillion in stimulus last year, nearly three times what they delivered during the global financial crisis.

Early, decisive action by monetary authorities proved a turning point for financial markets convulsed by the prospect of economic devastation.

Many central banks unveiled a series of innovative policies, crossing the point of no return in the process.

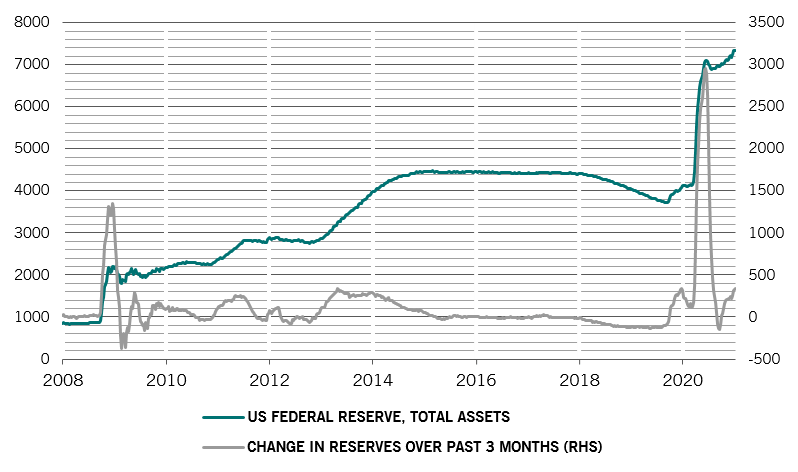

Fig. 1 - Stretching

US Federal Reserve balance sheet, USD billion

The US Federal Reserve, for example, established a facility on March 23 to directly purchase corporate bonds, including those downgraded to junk as a result of the pandemic.

This marked the end of the bear market, heralding a rare corporate debt issuance boom during a recession. Meanwhile, Australia joined Japan in implementing a pioneering yield curve control policy, buying as many bonds as necessary to achieve yield targets. Other central banks, including the Fed, are likely to follow in their footsteps. Helicopter money – channelling newly-created money to directly to households – cannot be ruled out either.

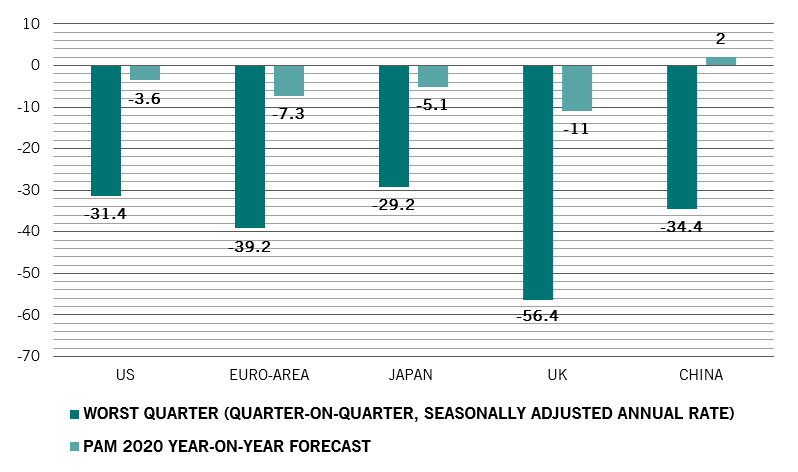

Depth of recession matters less than its duration

With the majority of mainstream asset classes turning in a positive performance in 2020, it is easy to forget that almost every major economy experienced its sharpest recession in more than a century or – in the case of the UK – more than three centuries. The lockdowns imposed to contain the virus during the first and second quarters of the year caused a decline in output of as much as 30 per cent on an annualised basis.

Even so, and contrary to the view prevailing during the pandemic’s first wave, economies have since experienced a remarkable V-shaped recovery, shrugging off the new restrictions put in place in the second half of the year to contain fresh virus outbreaks.

The US economy looks set to emerge from 2020 relatively unscathed, with output falling just 3 per cent compared to 2019 – a loss that is in line with previous recessions. China’s recovery has been even more impressive, with economic activity in almost every sector back above pre-pandemic levels.

Fig. 2 - A shock to the system

Maximum 2020 quarterly GDP decline and forecast full year GDP change , %

The lesson for investors, then, is that a deep but short recession is less damaging for markets than a shallow and long one.

A drawn out recession caused by systemic shocks is difficult for markets to get to grips with. It leaves deep scars, such as higher long-term unemployment, insolvencies and bad debts – problems that can take years to address. Slumps caused by short-term exogenous shocks, such as natural catastrophes, can be less problematic for investors as long as the right policy mix is in place. In 2020, investors saw a temporary shock (sharp fall in company profits) eclipsed by a permanent decline in bond yields (and, by extension, higher earnings multiples), resulting in a rise in equity markets.

What matters more to financial markets in such circumstances is the economy’s direction of travel rather than the pace of its expansion. Signs of a nascent recovery were already evident as far back as April; and with that, financial markets rediscovered their animal spirits.

For the EU, crisis is the mother of invention

Once again, those predicting doom for the EU were proved wrong. Confronted with yet another shock, the bloc managed to pull back from the brink. Unlike earlier crises, though, it wasn’t just the ECB stretching constitutional rules to organise a rescue. This time, Brussels broke precedent to launch fiscal measures that are likely to foreshadow further integration.

The situation looked bad in the spring. The pandemic had caused national EU governments to turn inward. Borders closed. There was competition for personal protective equipment and for a time it looked like Italy, one of the biggest member economies, would founder as its economy seized up. Meanwhile, the rumbling Brexit negotiations raised questions about which member state might be next to leave.

And yet, somehow, Europe’s politicians and technocrats came up with solutions. An EU-wide unemployment support scheme, SURE, was launched. But it was its NGEU recovery fund, a EUR750 billion scheme incorporating a mix of grants and subsidised loans to EU states with a focus on green investment, that proved truly transformative. Critically, both SURE and NGEU will be financed by bonds issued by the EU, making the bloc one of the largest bond issuers in Europe, on a par with the largest sovereigns. These bonds won’t replace German Bunds as a benchmark just yet, but it’s a first step.

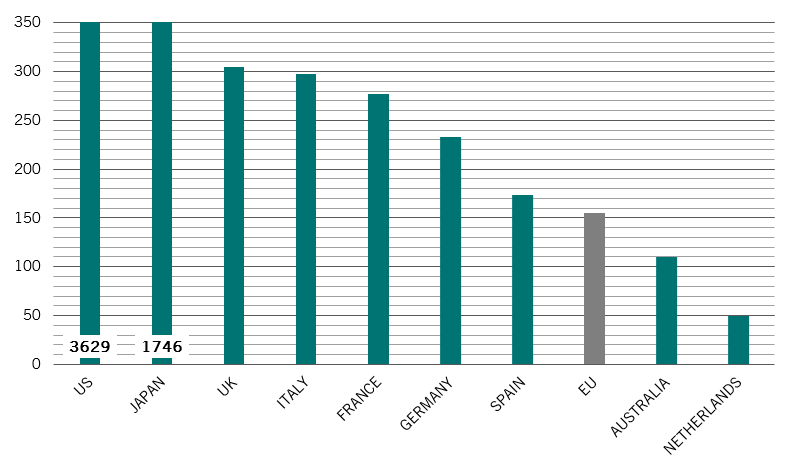

Fig. 3 - Borrowing binge

2021 gross bond issuance forecast, EUR billion

The ECB played its part too, of course, silencing the hawks in its governing council, and launching an emergency asset purchase programme, as well as offering ample subsidised liquidity to the banking sector.

True, the EU’s economy and equity market lagged those of the rest of the world last year. And 2020’s solutions don’t preclude another crisis. But no other member is following Britain to the exit. Increasingly, it’s clear that the EU is more durable than the sceptics credit. Indeed, Europe’s equity market has the potential to surprise this year given its attractive valuation and the heavy representation of cyclical industries in its stock indices.

ESG's march continues

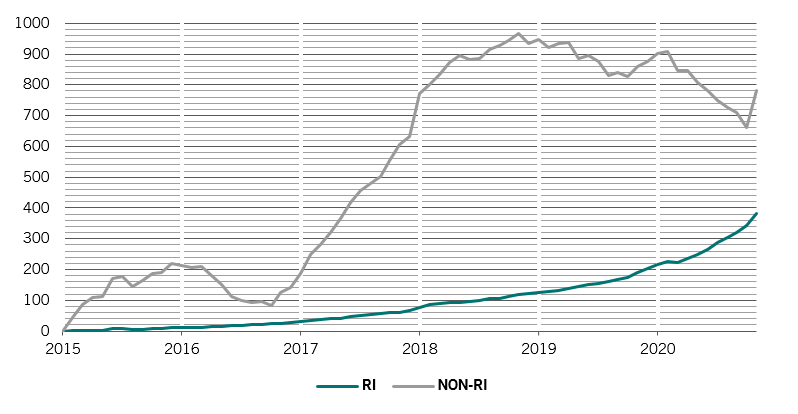

As the pandemic ravaged the global economy and financial markets, one trend truly proved its staying power – the growth of responsible investing.

Investors withdrew a significant amount of money from traditional equity investments during the worst of the crisis, yet exchanged-traded funds incorporating environmental, social and governance (ESG) factors saw over USD265 billion in net inflows globally – up more than five-fold from 2019, according to the Institute of International Finance. By the end of the year, assets held by global ESG funds topped USD1.3 trillion across all investment types.

Fig. 4 - The importance of being ESG

Cumulative inflows into global equity funds: RI* vs non-RI, USD billion

more from multi asset team

Barometer: A recovery we can believe in

As the rollout of Covid-19 vaccines continues apace, equity markets look set to enjoy strong support in 2021.

January 2021

Europe's defining moment

The EU pandemic recovery fund is a landmark deal that could transform Europe's economic prospects and revitalise its bonds, currency and stocks.

July 2020

What international investors can learn from China's pandemic recovery

September 2020

Globalisation after the virus

The coronavirus pandemic threatens to accelerate de-globalisation. But there are reasons to hope it won't.

April 2020

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.