Invest in Asian bonds: a large but extremely under-owned asset class

February 2021

Marketing Material

Investing in Chinese bonds

An emerging asset class of global significance

Share this article

A large but extremely under-owned asset class

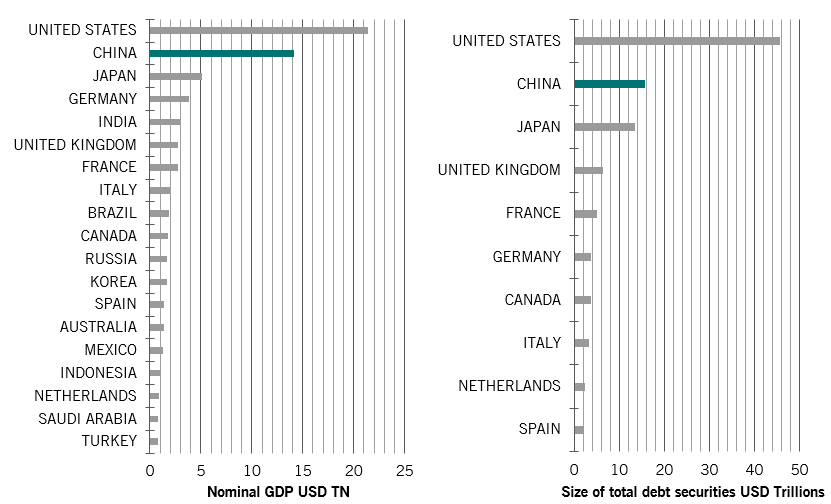

China is now the second largest bond market in the world with $15trillion in size, just after the US and before Japan1; yet it is still very under owned by international investors: foreign ownership of China bonds is still less than 3%2.

Second largest economy in the world & Second largest bond market in the world

Sources: Pictet Asset Management, IMF World Economics Outlook as of October 2020 / Pictet Asset Management, BIS, latest as of December 2020 based on Q2 2020 data

We believe this market is set to grow even more as China government bonds have been gaining global recognition via index inclusion such as in the Bloomberg Barclays Global Aggregate index or more recently in the JP Morgan GBI-EM Global Diversified index. Inclusion of China bonds into global bond indices can result in inflows of up to USD300bn3.

We also believe there would be an opportunity in China’s big corporate bonds market.

It is almost as big as the government bonds market already today and it is also developing fast4.

Traditionally Chinese companies have been financing via bank loans from the old command-economy days, which has two big drawbacks:

less transparency than corporate bonds market as it is a public market,

over-reliance on banking system.

Encouraging a deeper corporate bonds market is therefore in line with the Chinese authorities’ longer-term economic plan in the context of aging population, domestic pension demand, and a fast-growing domestic asset and wealth management industry.

Why invest in Chinese local currency debt?

With yields in global bonds market being at historical low, fixed income investors need an asset class that offers yield and resilience. We think that China bonds are a defensive diversifier to global portfolios with potential to enhance return for its merits of:

High quality, higher yield than developed market bonds

Low volatility, low correlation with other major asset classes

Today it is perhaps one of the only large chunk of assets within public bond market that still offers decent yield and decent quality.

High quality yield

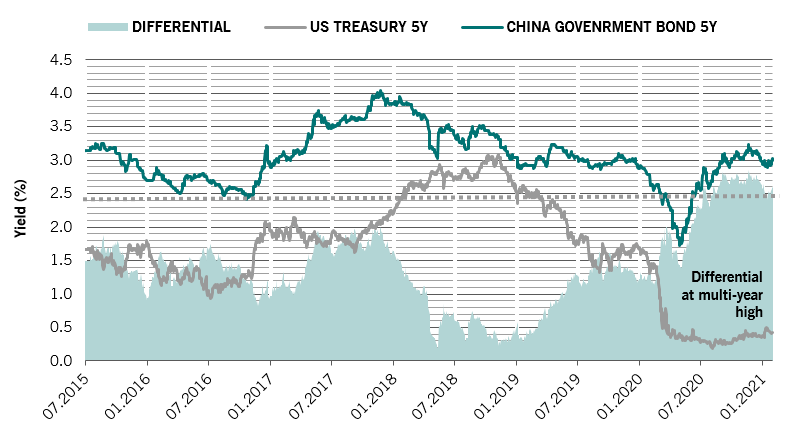

The asset class has an average A rated and low volatility while providing 3.5% of yield (in RMB terms) at the moment5. In addition, the yield differential between China government bonds and US treasuries (as well as other government bonds) is at multi-year high5.

Yield differential between China government bonds and US Treasuries is at multi year high

Source: Bloomberg, Pictet Asset Management as of January 2021

Shouldn’t China bonds’ yields stay at a premium above the US Treasuries as emerging market bonds, and why would this gap converge?

Decoupling from “emerging” assets

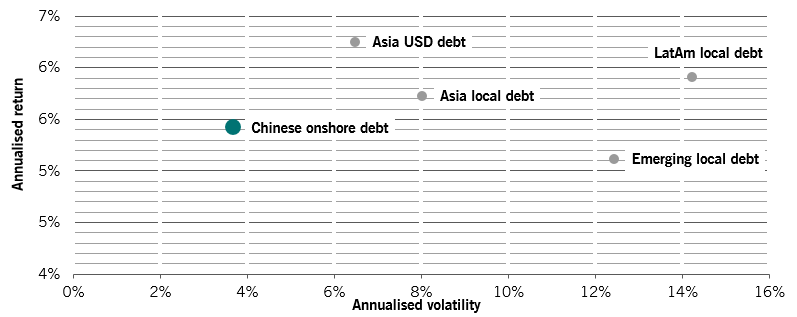

Investors have been looking at China bonds with a mindset of investing in emerging markets debt, but there are quite some difference. First of all China onshore debt is much larger than all other EM local currency debt combined. Secondly, It has delivered similar level of returns with much less volatility.

Traditional emerging markets normally see capital outflows, FX volatility in global risk off periods, but this has not been the case for China.

In our mind China bonds have been decoupling from Emerging assets and converging into a “core” fixed income assets. The pandemic having changed some of the dynamics, would only accelerate this trend.

China onshore debt has a favourable risk-return profile

Source: ChinaBond, JP Morgan; based on monthly data from 30 Sep 2005 to 31 Dec 2020. All indices are total return and in USD

We believe China bonds should be a defensive diversifier to global portfolios with potential to enhance return. Here are the reasons:

Resilience under global turmoil

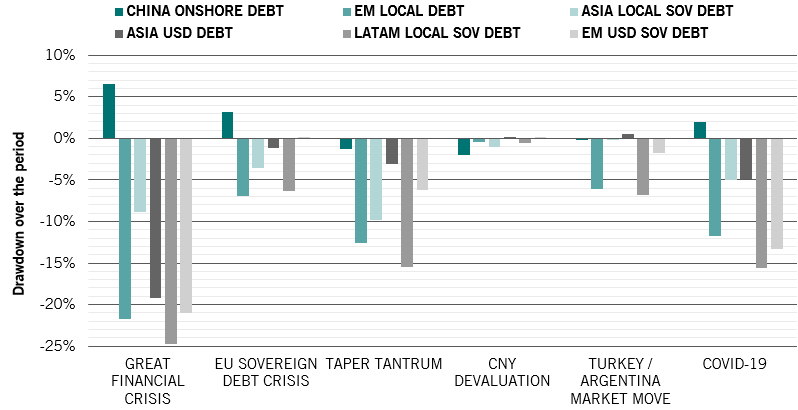

The asset class has proven its resilience in historical volatile periods including the 2008 financial crisis, the European debt crisis, as well as the Covid-19 crisis in Q1 20206.

Low / no drawdowns compared to other EM debt (EM local debt, Asia local debt, Asia USD debt, LatAm local debt & EM USD debt)

Source: Chinabond, JP Morgan. All indices are total return and in USD. Based on the following periods: Great Financial Crisis (Aug-Oct-2008); EU sovereign debt crisis (Aug-Nov 2011); Taper tantrum (8May – end 2013); CNY devaluation (10 Aug 2015); Turkey / Argentina move (Aug 2018); Covid-19 (21-Feb to 15-Apr-2020)

Converging to “core” fixed income assets

Chinese local bond have a low volatility – annually 4% (in USD) - compared to developed fixed income, emerging fixed income, developed equities and Chinese equities7. Added to its resilience and low correlation features, we think that it increasingly qualifies china bonds to become part of the “core” fixed income allocation for the yield to come.

Diversification advantage

It has a low correlation with major asset classes, including global bonds and equities; something very hard to find at this time where the majority of the public market asset classes are more and more correlate due to the current financials policies in place such as quantitative easing8.

The inclusion in global bond indices have encouraged inflows to the market consistently and the currency benefits from a relatively stable outlook as the RMB gradually marches towards a reserve currency.

Chinese local currency debt strategy

To capture the investment opportunities arising from this emerging asset class, Pictet Asset Management has developed the Chinese local currency debt strategy. Launched in 2015, the strategy is one of the first to offer clients access to the Chinese onshore bond market.

The team is fully dedicated to this strategy and developing the China bond franchise for the firm. Our team is a local team with local expertise: everyone involved in the strategy is truly bilingual, from portfolio manager, research analysts, traders, to risk manager.

We believe an active “sovereign + corporate” China aggregate approach, with a strong fundamental quality focus, should be the most suitable way for long term asset allocators to gain an efficient and comprehensive exposure to this large and growing asset class.

Pictet Asset Management’s commitment to the region

The region benefits from the full support from Pictet’s partners since inception, who envisage the longer-term demand from our clients on this big, emerging asset class with global significance.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.