How governments were placed on the eve of the coronavirus pandemic will play a significant role in how they emerge from the crisis.

Written by

Andres Sanchez Balcazar

Head of Global Bonds

Sabrina Khanniche

Senior Economist

Share this article

The global health crisis triggered by the coronavirus pandemic has firmly put the spotlight on how well countries will be able to handle the burden of rescuing their economies from an unprecedented meltdown. The question fixed income investors face is which countries will weather the storm and will sovereign debt crises follow?

Government deficits are ballooning everywhere, driven by two forces. First, huge fiscal programmes have been instituted to support households and companies at a time when many have seen incomes and revenues plummet due to the global lockdown. And, second, governments’ tax revenues have been hit hard by the dearth of economic activity, both domestic and cross-border.

So far governments have announced fiscal stimulus programmes in response to the coronavirus crisis worth 4.1 per cent of potential global GDP, nearly half of which will come from the US alone. Across the euro zone, the stimulus programmes are worth 3 per cent of GDP, while in Japan it’s 10 per cent. This spending necessitates huge volumes of government debt issuance. Central banks in the best-placed countries like the US, which benefits from reserve currency status, can absorb most, if not all, of this new debt through their asset purchase programmes. The US Federal Reserve’s balance sheet has expanded from USD4 trillion to USD6.5 trillion over the past couple of months alone and we expect it to peak at around USD8 trillion by the end of the year. In the UK, the Bank of England is pursuing an even more aggressive form of asset purchases by buying bonds directly from the Treasury in a form of debt monetisation – a policy that for long has been taboo.

But if the lockdowns last more than two quarters, a new set of fiscal measures will have to be adopted, which could mean solvency problems for some already highly indebted countries. We estimate US debt will have risen from 108 per cent of GDP to between 133 per cent and 145 per cent following its massive stimulus programme, worth some 7 per cent of GDP, depending on how sharply the economy bounces back. In the worst case, it could hit 165 per cent of GDP by the end of 2022. Elsewhere, higher debt levels are likely to ring alarm bells – it’s worth remembering that during the euro zone’s sovereign debt crisis, Greece flirted with ejection from the single currency as its debt breached 150 per cent of GDP.

Who's at greatest risk?

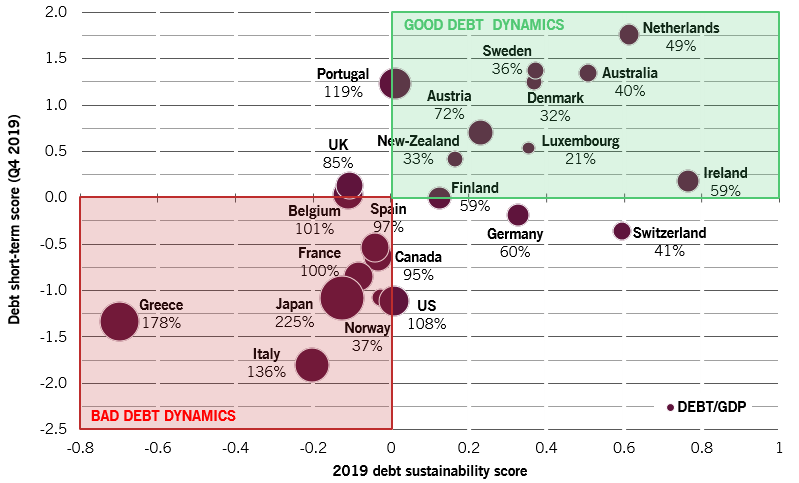

Pictet Asset Management’s sovereign risk scores show which countries were most vulnerable to dangerous debt dynamics coming into the coronavirus crisis. The metric is based on how countries stand relative to each other and to their own historic trend on three dimensions – how affordable their existing debt is, how well they’re able to finance it and the degree to which the debt will fall naturally as their economies grow.

Fig. 1 Developed sovereign debt dynamics

Pictet Asset Management short-term sovereign debt risk metric vs debt sustainability score (2019)

Debt dynamic scores are generated by Pictet Asset Management from a number of official indicators, comparing countries relative to each other and to their own trends. Source: Pictet Asset Management, CEIC, Refinitiv. Data are for 2019 for the structural sovereign scores and Q4 2019 for the short-term debt score.

Our analysis shows that Greece had by far the poorest state of debt sustainability at the end of 2019 among developed countries, followed by Italy, Japan, Belgium and the UK. At the other end of the scale, Switzerland, the Netherlands and Ireland were in the most enviable positions.

Mapping countries’ short-term debt situations against their structural scores confirms that Greece, Italy and Japan exhibit the worst debt dynamics, though France is also a worry. By contrast, other northern European and Scandinavian countries are in a good position.

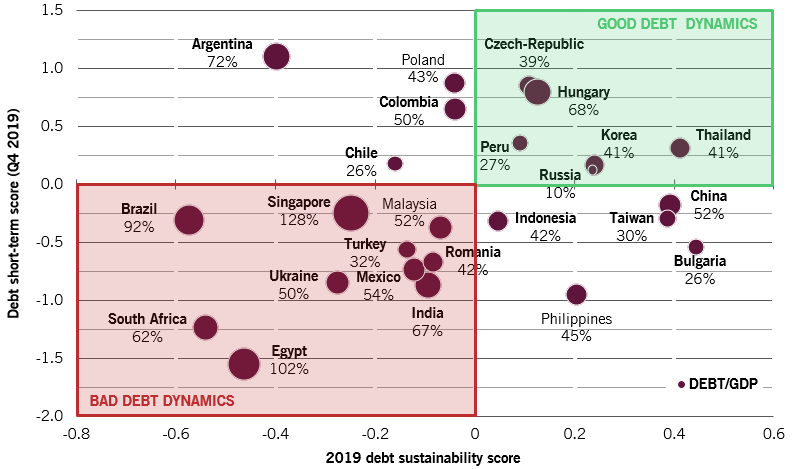

Fig. 2 Emerging sovereign debt dynamics

Pictet Asset Management short-term sovereign debt risk metric vs debt sustainability score (2019).

Source: Pictet Asset Management, CEIC, Refinitiv. Data are for 2019 for the structural sovereign scores and Q4 2019 for the short-term debt score, excluding China for which structural sovereign score is for 2018 and short-term debt score is for Q4 2018, Bulgaria for which short term debt score is Q4 2018, and Egypt for which short-term debt score is Q3 2019.

Among emerging economies, the countries that faced the biggest risks to their sovereign debt at the start of the crisis were Brazil, South Africa, Egypt and Argentina. In terms of debt dynamics relative to short-term debt situations, South Africa, Egypt and Ukraine are of greatest concern. Those likely to be most resilient were Russia and Korea.

Flashpoint

Italy was a flashpoint during the euro zone crisis and it could prove to be one again. Italian government debt could potentially hit 150 per cent of GDP by the end of this year. The European Central Bank already owns Italian bonds worth some 22 per cent of Italy’s GDP and, as such, it has a big role in the sustainability of the country’s debt. The ECB has already said it would take a flexible approach to purchases of member states’ bonds and will be absorbing some 90 per cent of net new issuance by the single currency region’s governments this year.

Those purchases by the ECB come against the backdrop of northern European concerns about creeping debt mutualisation. But ultimately, if the euro zone is to be kept together, some sort of debt pooling will be necessary – extend and pretend can only be supported for so long before the market tests the region’s political resolve. We expect that there will be moves in the direction of mutualisation, which ensure that yields on Italian bonds stay contained.

The ECB faces a fine balancing act in how it navigates the coming months.

The ECB, however, faces a fine balancing act in how it navigates the coming months and will have to be deft in how it applies game theory. It wants to prevent another sovereign debt crisis. But it also doesn’t want to entirely remove pressure on euro zone politicians to reach agreement on some sort of debt mutualisation. If the central bank is too accommodative and compresses southern European government bond spreads too much, this would lessen the need for euro zone governments to agree on how to move forward.

An even more immediate concern is that some emerging market economies have already run out of monetary headroom. Inflation won’t be an issue for some time in developed economies as depressed demand and weak oil prices drag down consumer prices overall, notwithstanding aggressive central bank action. In some emerging economies, however, central bank policies are already acting to drag down their currencies in what could turn out to be another devaluation/inflation cycle. Worryingly some large developing economies – Turkey, Brazil, South Africa – are heading in this direction.

The global pandemic is likely to expose strains that already exist in the global economy as well as throwing up new problems. How governments came into the crisis will play a big role in how they emerge.

Andres Sanchez Balcazar joined Pictet Asset Management’s Fixed Income team in 2011 and is Head of Global Bonds. Before joining Pictet, he was a senior portfolio manager for Western Asset Management Company LTD for six years. During this time he was responsible for global, European and absolute return fixed income portfolios. Previously, he worked for five years as a global and European portfolio manager with Merrill Lynch Investment Managers. Andres started his career in 1997 at Banco de la Republica de Colombia, where he provided macroeconomic analysis on the US, Europe and Japan. Andres holds a degree in Economics from Universidad de los Andes and a Master's in Management from HEC Paris. He is also a Chartered Financial Analyst (CFA) charterholder.

About

Sabrina Khanniche

Sabrina Khanniche joined Pictet Asset Management in 2011. She is a Senior Economist, Lead on Eurozone and MEA.

Before joining Pictet, she was with Groupama Asset Management during four years as a Financial Engineer in charge of the analysis and modelling of hedge fund risks. In this regard, she published and presented her work in international academic conferences.

Sabrina holds a Master and a PhD in Economics from the University of Paris West Nanterre La Défense.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.