The inclusion of renminbi-denominated debt in the flagship global benchmark bond index will transform the asset class into a strategic investment.

Written by

Cary Yeung

Head of Greater China Debt

Share this article

For all the turmoil caused by the coronavirus, one corner of China’s financial market could prove surprisingly resilient: local currency debt.

This is because the country’s onshore renminbi (RMB) -denominated bonds are about to be included in JP Morgan’s flagship emerging market bond index for the very first time.

This is a landmark moment, both for China and for investors worldwide.

For authorities in Beijing, it's a stamp of approval for their efforts to liberalise the country's capital market and integrate more into the international financial system.

For investors, it opens up a new world – one where the RMB becomes a genuinely global investment currency. In a matter of months, China's USD13 trillion onshore bond market will play a far greater role in bond portfolios.

RMB bonds and reserve currency

Foreign ownership of Chinese bonds was already rising in anticipation of the index change, which the International Monetary Fund expects to result in capital inflows of as much as RMB7.4 trillion.

Non-Chinese investors built up their holdings of RMB debt to RMB2.2 trillion by September 2019, up from RMB700 billion in mid-2017. Foreign central banks and sovereign wealth funds account for the biggest share with 58 per cent of that total - asset managers and commercial banks currently hold 20 per cent1.

Thanks to central bank purchases, the RMB is now the world’s fifth largest reserve currency, making up just under 2 per cent of the total foreign exchange reserves. If that share were to double, it would amount to an additional RMB1.5 trillion of RMB bond investments, the IMF says.

According to Pictet Asset Management's economists, it won’t be long before the RMB’s share of international reserves is greater than that of the British pound2.

Inflows from private investors will also expand rapidly as other index providers follow in the footsteps of JPMorgan to incorporate the asset class into bond benchmarks.

Index inclusion also brings into relief the asset class's positive attributes at a time when a large volume of bonds – in developed and some emerging economies – yield below zero.

The yield on five-year Chinese government bonds stands at 2.8 per cent, compared with 1.4 per cent for US Treasuries, -0.1 percent for Japanese Government Bonds and -0.6 per cent for German Bunds with the same maturity3.

Yield is not their only selling point. They also offer diversification. The returns of RMB bonds do not correlate especially strongly with any major global asset class – bond or equity. The correlation of RMB bond returns with those of US and European bonds and equities is less than 0.34.

Add in the currency's potential for appreciation over the long run (see our previous article) and investors will find the market difficult to ignore for long.

Burgeoning asset management industry

Already, global asset managers are becoming a significant source of investment flows into the RMB bond market. In the first eight months of 2019, they vaulted public sector investors to become the largest net foreign buyers of Chinese onshore bonds, accounting for 51 per cent of net bond purchases – or RMB110 billion in nominal terms5.

Making it easier still for foreigners to access the market is the “Bond Connect” programme, which has allowed non-Chinese investors to trade in Hong Kong without an onshore account since its launch in 2017. The programme’s trading volume has risen nearly 200 per cent in 2019 to RMB2.6 trillion6.

Policymakers are also keen to attract foreign funds to hasten the development of a home-grown asset management industry.

This is a priority for China as the country’s rapidly aging population demands a sustainable pension system.

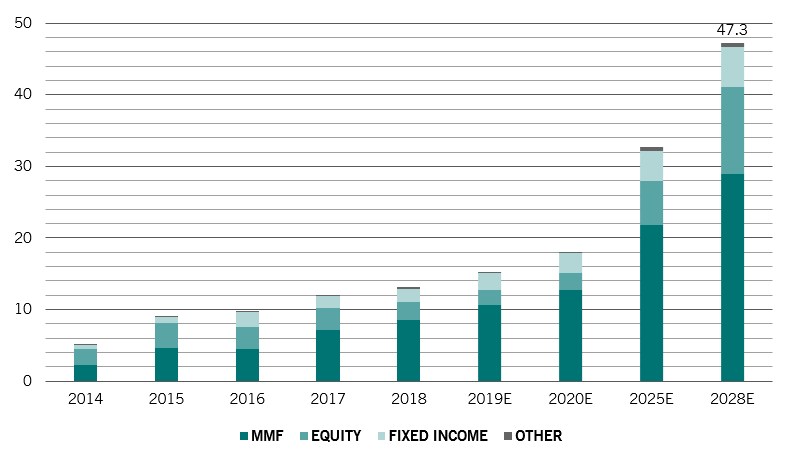

China’s asset management industry – fund houses, insurers and securities and trust companies – is expected to triple in the 10 years to 2028 to RMB47.3 trillion as Beijing is set to remove all foreign ownership restrictions later this year.7

This should also help broaden the domestic institutional investor base currently, which is currently dominated by commercial banks.

Opportunities multiply

AUM growth of China's asset management industry by asset class, RMB trillion

Source: iFinD, Roland Berger

More policy easing

The RMB debt market’s elevation to international status comes at time when monetary conditions at home are particularly favourable.

The People’s Bank of China has cut the reserve requirement ratio – or the amount of cash that all banks must hold as reserves – eight times since early 2018 to arrest an economic slowdown. Earlier this month, the PBOC lowered the interest rates on reverse repurchase agreements and injected more liquidity into money markets to relieve pressure on the economy from the coronavirus outbreak.

We expect monetary conditions to ease further. Measures designed to support struggling industries should form part of the policy mix.

It’s been a tough start, but the Year of the Rat still promises to bring strong growth for the onshore RMB-denominated debt.

Cary Yeung joined Pictet Asset Management in 2014 as Head of Greater China Debt. Previously, Cary worked at Taikang Asset Management in Hong Kong, where he was Head of Fixed Income and portfolio manager for a range of Asian fixed income products. Before that, he worked at UBS Global Asset Management Hong Kong and Prudential Asset Management Singapore as a senior portfolio manager for various Asian fixed income portfolios. Cary started his career with PWC and then KPMG, before moving to First State Investments where he was a Credit Analyst. Cary graduated with a Bachelor of Business Administration (Finance and Accounting) from Simon Fraser University, Canada. He is a Chartered Financial Analyst (CFA) charterholder and a Certified Public Accountant. Cary is fluent in English, Mandarin and Cantonese.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.