For non-life insurance companies, bonds are an investment staple. And for good reason. Insurers’ liabilities – current and future expected losses from claims – tend to be of short duration, between two to four years on average.

Which means the ideal return-generating, or liability-matching, asset is one that is exceptionally liquid, produces stable streams of income, and holds its capital value.

The trouble is, fixed income markets are not as dependable as they used to be.

In fact, in the decade since the US housing market crash, fixed income investors have had to abandon several of the beliefs they once held dear. It turns out, for instance, that negatively-yielding bonds are no longer an absurdity. Thanks to sustained quantitative easing, the volume of fixed income securities trading at negative yields has never fallen below USD6 trillion since 2016. (The figure leapt to as high as USD17 trillion in September last year).

Also consigned to history is the notion that developed government bond markets are oases of calm. On one eventful day in May 2018, the yield on Italy’s two-year bond spiked by more than 150 basis points, the sharpest one day sell off in more than 25 years. This was preceded by the US 'flash crash' of October 2015, which saw yields on 10-year Treasuries move up and down by 160 basis points within just 12 minutes. As the US Federal Reserve warns, such episodes will be more frequent in future as passive investing and algorithmic trading gather pace.1

(The extreme moves seen in the wake of the coronavirus outbreak -- equities and corporate bonds selling-off sharply and government bond yields dropping dramatically -- testify to this new, more volatile market climate).

Fixed income investors have had to abandon many of the beliefs they once held dear.

On top of wafer-thin yields and higher bond market volatility, insurance companies face an added complication. The definition of a diversified bond portfolio has also had to be torn up. That’s because the various fixed income asset classes that constitute the global bond market2 have been tracking one another more closely in recent years. The correlation of the returns of US Treasuries, corporate debt and US dollar-denominated emerging market bonds has been higher in the past three years than in the past 10.

It is unlikely that insurers can accommodate this new reality for much longer. Holding a more volatile portfolio, or one that contains a greater proportion of higher yielding but lower quality bonds, is an impractical and potentially risky option. Not least because regulations such as Solvency II have made it costly for insurance firms to hold riskier assets.

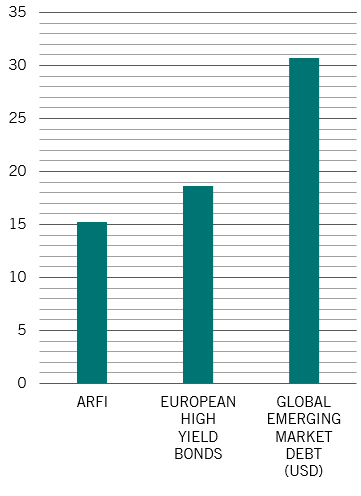

But there is an alternative to traditional bond portfolios, and comes in the form of an absolute return fixed income (ARFI) strategy.