Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Covid and the spectre of stagflation

Will huge amounts of stimulus trigger the sort of stagflation that ravaged the world in the 1970s? We don't think so.

Written by

Patrick Zweifel

Chief Economist

The vast volumes of money central banks have pumped into the global financial system to contain the economic impact of the Covid pandemic have raised the spectre of inflation. Could these ignite uncontrolled price pressures? Or, worse still, the sort of debilitating stagflation that swept significant parts of the world during the 1970s? We don't think they will.

Experience of the past decade has made it clear that quantitative easing (QE) isn’t a straight path to rising consumer prices. For many, however, current inflation fears hinge on the fact that central bankers’ latest measures are in many cases far in excess of the QE that was launched in the wake of the global financial crisis. Increasingly, they are buying private assets and de facto monetising huge government deficits. The fear is that monetary and fiscal stimulus – respectively half and three times as big again as in response to the global financial crisis – could yet prove to be inflationary fuel.

The good news is that Covid is unlikely to lead to the stagflation that gripped the world during the energy crisis of the 1970s.

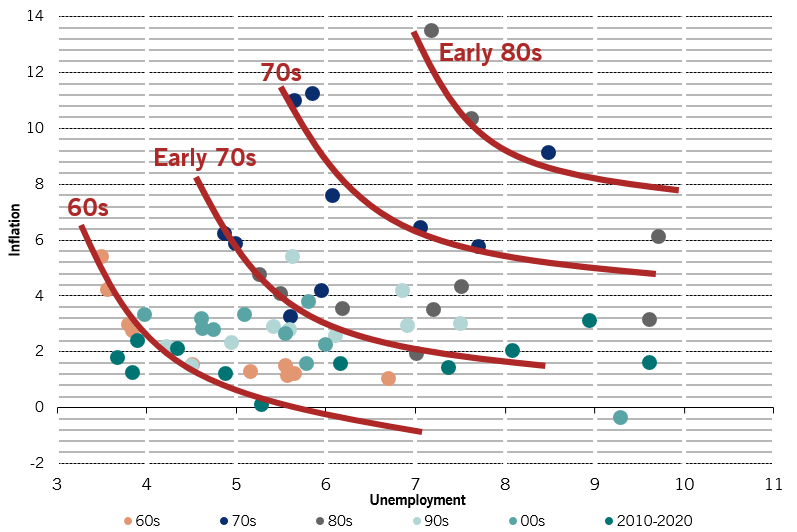

Phillips curves

The estimated relationship curves between US inflation and unemployment rates for various periods. Dots represent average unemployment and inflation rates for given years, according to legend.

The combination of fast rising prices and high unemployment was unique to the circumstances of 50 years ago, which don’t seem to be mirrored in current events.

The 1970s stagflation was largely triggered by two oil shocks – the first precipitated by the 1973 Yom-Kippur War, the second by the 1979 Iran Revolution. Developed economies’ high degree of dependence on oil – output then was much more heavily geared to manufacturing and industrial production – meant that these price spikes quickly fed through the economy. These days their average dependence on oil is only a little more than a third of what it was in 1972.

The fallout back then was amplified by several other factors. Food made up a much bigger part of people’s consumption basket, and was particularly sensitive to oil prices, not least through the cost of oil-based fertilisers. In the US, price controls were abandoned by 1973, while the low unemployment rates at the start of the decade gave workers the leverage to negotiate inflation-busting wage rises and restrictive measures that made it expensive to hire workers during the economic crisis later on.

In the UK, authorities tried to offset the oil shock with accommodative monetary policy, which merely accelerated inflationary pressures. The Swiss, on the other hand, did the opposite, which helped to moderate inflation there. So while prices jumped everywhere, it was worst in the UK and least bad in Switzerland. For its part, the US took a neutral monetary line, resulting in two inflationary spikes, averaging at more than 7 per cent over the decade and with a peak at some 14 per cent.

Shifting the Phillips curve

As inflation expectations became embedded, the trade-off between prices and unemployment – known as the Phillips curve – worsened. A given level of inflation became associated with ever higher unemployment before severe monetary measures finally suppressed price pressures and returned expectations to more moderate levels.

The question now is whether the Covid pandemic’s impact on economies is similar to that seen during the 1970s. We don't think so. For one thing, the current supply shock isn't like the oil shock of fifty years ago for which the economy then was ill prepared. But that doesn't mean there are no risks.

Two sorts of supply shock seem possible. First, workers could demand higher wage settlements in anticipation of rising inflation, which would threaten to feed a negative spiral. This could be reinforced by ever higher minimum wages as politicians bow to populist pressure. Second, some goods and services could become more expensive as producers respond to new regulations imposed by public health concerns – such as rising restaurant bills and transportation costs to reflect social distancing needs. Deglobalisation could further damage supply networks and impose rising costs. Import restrictions now cover 7.5 per cent of global trade from less than 1 per cent in 2009.

The good news is that Covid is unlikely to lead to the stagflation that gripped the world in the 1970s.

Meanwhile, stimulus could yet stoke a surge in demand. Especially since, unlike a decade ago, banks now are in much ruder health, making them much more willing and able to pass the liquidity on to the wider economy in the form of credit creation. At the same time, a bigger proportion of today’s stimulus is directed to the end-users, households and businesses.

But the degree to which the stimulus is likely to be inflationary depends in large part on people’s expectations of future inflation. Higher expected inflation prompts rising spending which increases how fast money circulates, which pushes up prices and boosts inflation further. But with interest rates at zero, reflecting what’s known as a liquidity trap, it becomes hard for this cycle to kick in. That’s because there is no cost to holding money and thus no strong push to start it circulating – so the velocity of money stays low.

Ultimately, all this stimulus could boost output ahead of the economy’s potential. That could happen if measures to control Covid cause productivity to fall. Or, more likely, if policy responses were overdone as may be suggested by the recent surge in US household income – at 13.4 per cent on the month, that’s twice the size of the previous largest increase which came in May 1975. In that case, inflation could well rear its head again. But that’s not a risk we see in the near term. And certainly not a return to the 1970s.

Related articles

Globalisation after the virus

The coronavirus pandemic threatens to accelerate de-globalisation. But there are reasons to hope it won't.

April 2020

Barometer: Equities out of step with economy

While economies are beginning to emerge from lockdown, market hopes for a V-shaped recovery look optimistic.

June 2020

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.