Overview: diverging fates

Luca Paolini's Outlook for 2020

Tread carefully. The path to strong investment returns in 2020 won't be a smooth one. Global economic growth is lacklustre and valuations for most major asset classes look stretched. Add in the risks around trade wars and the US presidential election, and we believe global equities will only manage to deliver single digit returns, while most developed market bonds will fare even worse.

Investors should expect a significant divergence in the returns of individual asset classes.

We believe 2020 will mark the end of the bull run for the US dollar – and with that the leadership of US equities. In contrast, value stocks, European equities and emerging market debt have the potential to outperform.

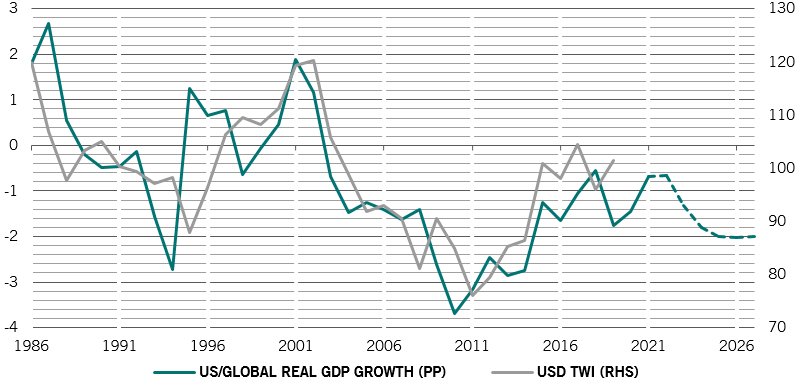

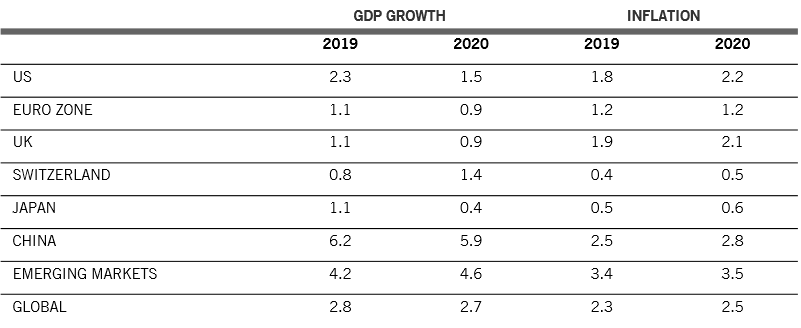

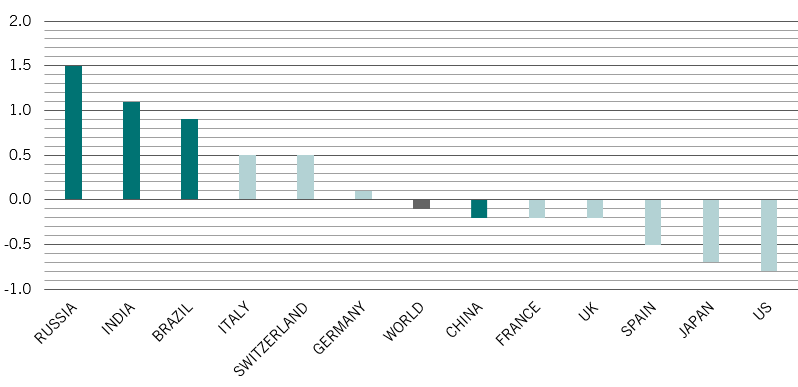

This view is supported by our business cycle indicators. On a global level, they suggest that growth will slow slightly next year, to around 2.7 per cent annualised – 20 basis points below potential. But this masks widely different regional prospects (see Fig. 1). Most developed economies, particularly the US, will see a slowdown in growth. We forecast that the US expansion will slow to 1.5 per cent in 2020 – the weakest in a decade, and do not rule out the possibility of a very shallow technical recession in the first half. In contrast, emerging markets such as India, Brazil and Russia should see an acceleration.

As a result, we expect that the difference in the pace of growth between developed and emerging economies will reach 340 basis points – a seven year high. The US slowdown will also erase the North American economy’s advantage over Europe, to the benefit of European equities and the euro.

Inflation should remain contained, enabling major central banks to continue monetary stimulus, albeit it a slower pace than in recent years. We expect central banks in US, Europe, Japan and China to increase liquidity provision by a total of USD1 trillion next year – an attention-grabbing amount, but 20 percent below the average injections of the past 11 years.

Some of that shortfall may be filled by fiscal stimulus. Notably, in traditionally frugal Germany, there are signs that the political mood is slowly shifting towards increased spending. However, we believe that globally the peak in fiscal stimulus was reached at the end of 2018. Current budget projections in both China and the US do not leave room for any significant new measures.

The prospect of slowing US growth and limited scope for stimulus bode badly for the dollar, whose valuation looks very stretched. According to our models, the greenback is about 20 per cent overvalued and we expect this premium to be steadily erased over the coming five years. That in turn should benefit emerging market assets.

The US is also one of the most expensive equity markets in our model – something that will become harder to justify against a backdrop of virtually flat corporate earnings, a slowing economy and a rate-cutting US Federal Reserve.

In contrast, we see some value in US Treasuries (especially in inflation linked paper), emerging market currencies and in value stocks – companies that trade at a lower price than implied by their dividends, earnings or sales.

Technical indicators show that investors are already in a relatively cautious mood. In the first 10 months of 2019, investors pumped a net USD400 billion into global bonds, while withdrawing USD221 billion from equities, according to EPFR data. Equity allocations remain close to their lowest levels in a decade. While we believe the caution may well be warranted, such positioning should put a floor under the equity market over the coming months, ensuring that while returns will be modest they will mostly still be positive.