When the US economy does roll over there's little prospect of a fiscal safety net. America Inc is unlikely to come to the rescue either.

Written by

Patrick Zweifel

Chief Economist

Steve Donzé

Senior Macro Strategist

Share this article

Is the US economy running headlong towards a cliff? The good news is that if it is, it’s got a way to go – there isn’t likely to be a reckoning for at least the next 12 to 18 months.

Unfortunately, when the economy does end up flailing over empty air like the cartoon character Wile E. Coyote, there’s little prospect of a fiscal safety net. As former US Federal Reserve chairman Ben Bernanke recently warned, President Donald Trump’s spending bonanza is badly timed, coinciding with record low unemployment. And the sugar rush from the stimulus is likely to fade around the same time as the Fed’s interest rate hikes will have the greatest impact on the economy, between late 2019 and early 2020.

The current US economic recovery is already the second longest on record. Since the previous trough in June 2009, there have been 108 months of unbroken growth. Only the March 1991 to March 2001 boom was longer. That’s got many people wondering how much longer this cycle can last.

An imminent end to the expansion is unlikely. That’s because previous downturns were typically flagged by two major developments that have yet to materialise. Those are, first, a boom in private sector, and particularly household, debt and, second, a collapse in the yield spread between 10-year and one-year US Treasury bonds.

At the start of the global financial crisis in 2008, the US household debt to GDP ratio stood at a shade under 100 per cent. It has since dropped to around 80 per cent, having levelled off during recent years. Even with rising interest rates, which push up debt servicing costs, US households are relatively comfortable.

The picture might be slightly less positive when it comes to corporate borrowing. Non-financial corporate debt is at a historic high of more than 73 per cent of GDP, up from post-crisis levels of just under 66 per cent. But here too there’s no reason for immediate concern. Trump’s tax reforms have boosted US corporate earnings while also removing incentives to take on additional debt.

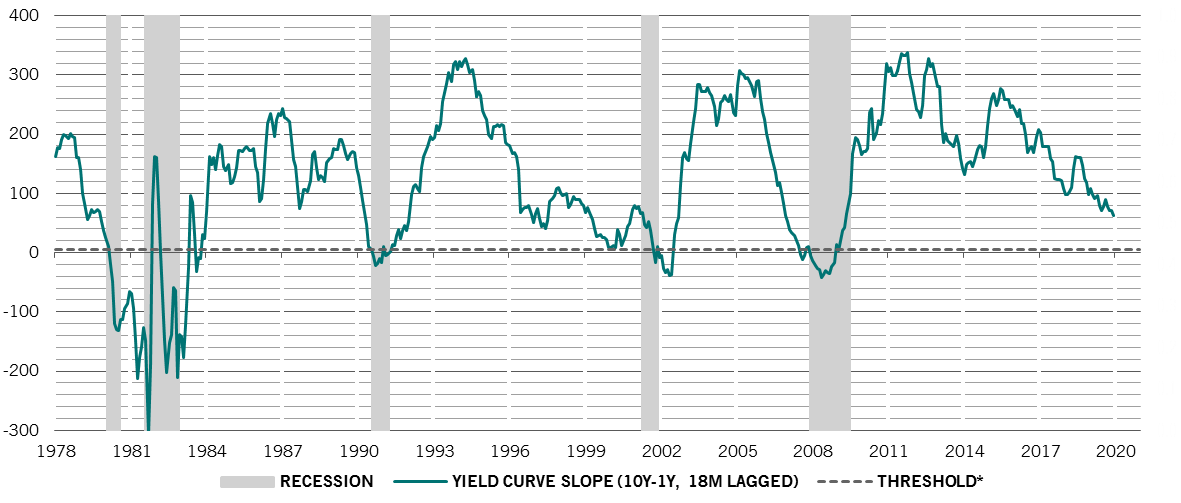

Wiggle room

US Treasury bond yield differentials, 10Y - 1Y, basis points

*Optimal threshold determined such that the benefits of hits equals the costs of misses

Source: Pictet Asset Management, Thomson Reuters Datastream. Data from 01.10.1976 to 19.06.2018

Meanwhile, although spreads between 10-year and one-year Treasury bonds have been dropping with the tightening of Fed policy, there are no signs of immediate danger here either. Typically, our models show that a fall in the spread to five basis points suggests recession will unfold 18 months from that point. Right now, the spread is 63 basis points, which is roughly where it was in the mid-1990s, when the cycle had much longer to run.

Overall, the model suggests the contemporaneous probability of recession is just 3 per cent (although it’s worth remembering that recessions tend to be identified with hindsight and sometimes only after a delay of several quarters).

When the expansion does end, however, America Inc is unlikely to come to the rescue. That’s because American corporations appear especially reluctant to invest, preferring to save or return the cash to shareholders.

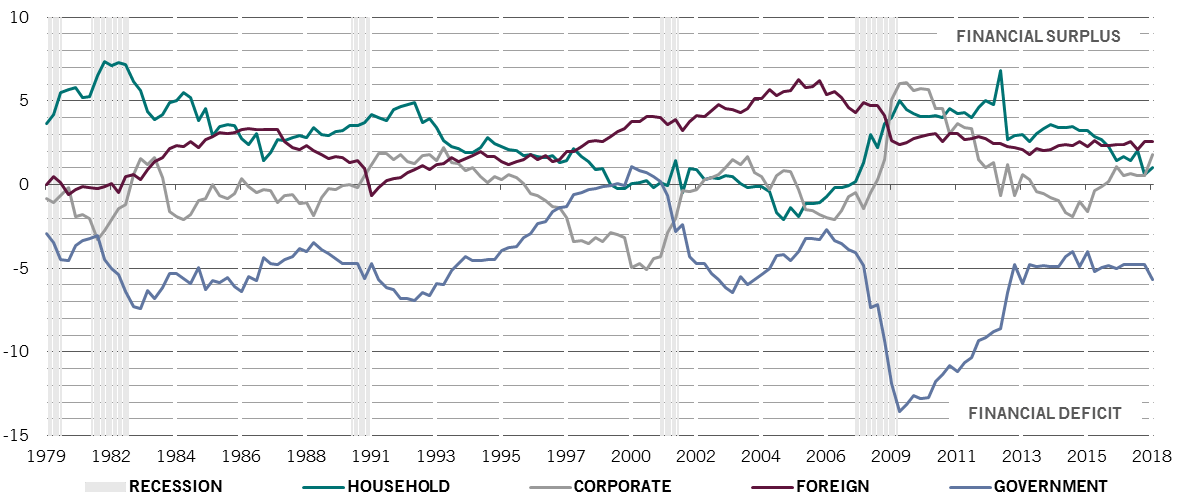

Our analysis of the US's financial balances shows that the public sector is the only one that has been in deficit in the most recent quarter, with all the others – domestic households and companies, as well as foreign investors – firmly in savings mode. Corporate America's financial surplus is particularly elevated, standing at 1.8 per cent of GDP, the highest since 2010 (see chart).

It's a balancing act

US quarterly financial balances, as percentage of GDP

Source: The Federal Reserve, Pictet Asset Management. Data covering period 01.10.1979 - 31.3.2018

Other data show a similar picture, with total non-residential corporate investment in the US standing at 12.8 per cent of GDP, below the average pre-crisis level of 13.2 per cent.

Such a distribution of financial balances is highly unusual at this point in the US economic cycle. It is usually seen in the immediate aftermath of a recession, when the government stimulates the economy with increases in public spending to offset a decline in spending and borrowing among households and businesses.

The imbalance is going to get worse from here – the IMF expects net US sovereign borrowing to hit close to 6 per cent of GDP next year. The question is who picks up the tab.

Given simmering trade tensions between Washington and its partners, it is unlikely that the US could count on foreign investors to finance its spending. For the accounts to balance, this leaves domestic companies and households having to take the slack. But by saving more, they’ll be consuming even less.

In extending its fiscal deficit, the government is outbidding companies for financing – in other words, the state is crowding out private investment activity, a phenomenon that tends to weigh on growth.

So while the government’s spending may help to prolong the current economic upswing, it could also exacerbate the pain when the recession finally arrives.

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management, having assumed the position in 2009. Before that, he was head of the “Macro Research Team” at Pictet Private Wealth Management, where he was responsible for emerging markets and Japan, and for the development of quantitative models on major asset classes. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in Econometrics from the University of Lausanne.

About

Steve Donzé

Steve Donzé joined Pictet Asset Management in 2007. He is Deputy Head of Investment & Products for Pictet Asset Management Japan, part of the Multi Asset unit.

Previously, he was a Senior Macro Strategist in the Swiss Multi Asset team, co-managing a range of multi asset flexible strategies.

A member of Pictet Asset Management Strategy Unit, he engages in public debate on monetary policy-making.

Prior to Pictet, he held positions at the Swiss Bankers Association and the Swiss Ministry of Foreign Affairs.

Steve holds a Master’s degree from the Graduate Institute of International and Development Studies and a PhD from the London School of Economics.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.