Asset allocation: a fine balance

China remains ahead in terms of the extent of its recovery, which, along with a weaker dollar, should be supportive for emerging markets and for the materials sector.

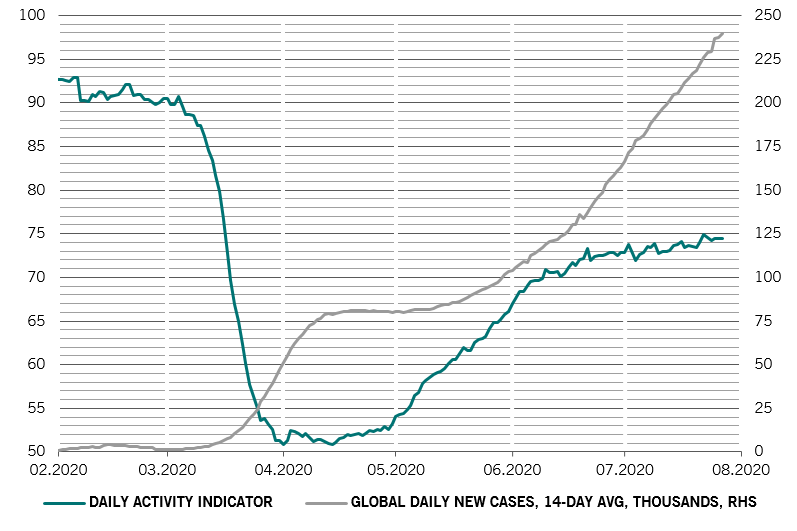

However, daily indicators, such as credit card use and traffic congestion, suggest that on a global level activity is improving slowly, potentially reflecting a fresh increase in Covid-19 cases (see Fig. 2).

In general, we think that the monetary and fiscal stimulus pledged across the globe should be enough to offset the uncertainty related to the pandemic. In the US, for example, government transfers now account for around a quarter of total household income – more than double the pre-Covid level. That may lead to problems further down the line if normal sources of income do not recover, but for now should provide a valuable safety net for the economy and for markets.

The global recovery so far, albeit better than previously anticipated, has been led by improving private consumption. Industrial production has remained muted, hence running down inventories. Going forward we expect inventory levels to stabilise and gradually pick up again, with increased production underpinning the next phase of recovery in growth.

Liquidity is still extremely abundant, with all major economies scoring "double plus" in our model. Japan is the latest major developed economy to join this club following a sharp increase in loans under the government’s guarantee programme. We expect the central banks of the world’s top five economies to inject the equivalent of 14 per cent of GDP in monetary stimulus this year, almost double the post-GFC peak. But the pace has flattened out recently and a peak in the global easing cycle is likely not far off. It may even come this quarter. On our analysis, the market is already almost fully discounting the projected evolution of liquidity creation over the rest of the year – including a formal yield curve control policy from the US Federal Reserve.

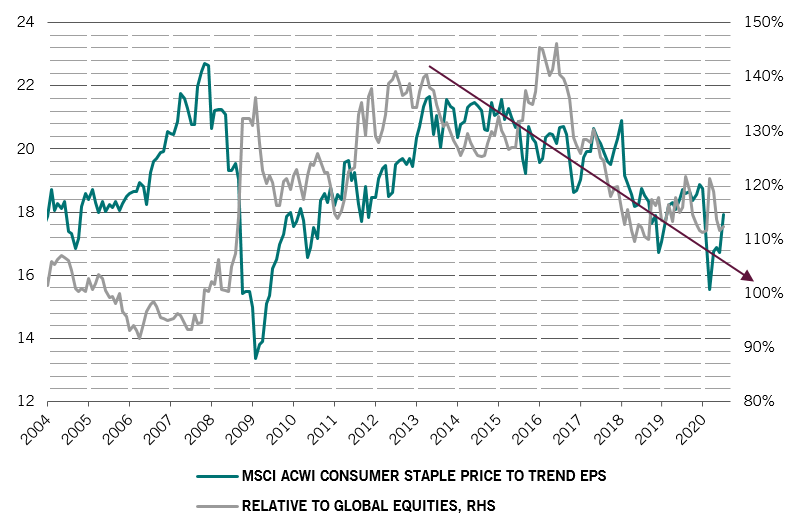

Indeed, markets have discounted so much good news that valuations are looking rather stretched. Global stocks have gained over 40 per cent since March. Now, for the first time since September 2018, they are flashing expensive relative to their own 20-year history, according to our models. The price to trend earnings ratio on MSCI All Country World Index has climbed to 16 times – close to its pre-Covid crisis levels and up from 12.3 in March. At the same time, we believe that risks to earnings are still very much tilted to the downside.

However, bonds look even more expensive, offering the worst value in two decades. Yields on US inflation linked-bonds (TIPS) and investment grade credit have both fallen to record lows.

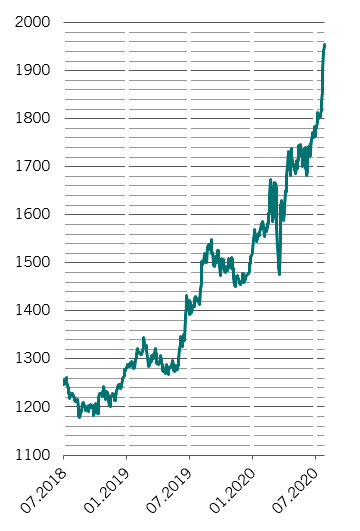

Gold is at all-time highs in absolute terms (if not yet when adjusted for inflation). However, shining fundamentals and demand for diversifying assets suggest there is further to go. We remain overweight on gold, expecting it climb to USD2,500 an ounce by 2025, from USD1,960 currently.

Encouragingly technical charts show that speculative positioning in gold is relatively light considering the extent of the rally. Sentiment indicators, meanwhile, support our neutral stance on equities while pointing to a temporary pause in the credit rally.