Strategic credit: a nimble approach for an uncertain world

Jon Mawby discusses the advantages of active credit allocation in portfolios now that government bonds no longer serve their traditional purpose.

Written by

Jon Mawby

Co-Head of Absolute & Total Return Credit

Governments have launched massive efforts to underpin their economies in the wake of the Covid crisis. What are the most important implications for bond investors?

To begin with, investors need to rethink the role of bonds in their portfolios. That’s because government bonds no longer fulfil their historic role. They don’t provide a steady and secure income, nor are they a safe store of value, or, indeed, a source of diversification to equities. As a result, a traditional portfolio constructed of 60 per cent equities and 40 per cent bonds, with the bond allocation tilted towards government securities, no longer makes sense.

In fact, if central banks are successful at pushing up inflation and then return policy to more normal levels, including raising interest rates, investors run the risk of suffering losses on both their bond and equity holdings. So, they need to re-think how they construct portfolios.

Is it really reasonable to fear inflation? After all, major central banks have consistently been undershooting their 2 per cent inflation targets for most of the past decade.

In considering this, it is worth bearing a few things in mind. First, although central banks introduced QE and other emergency measures after the 2008 financial crisis, their response was largely focused on underpinning the banking sector. Second, that intervention was considerably smaller than what they’ve done this year. Our economists estimate that liquidity injections then were worth around 8 per cent of global GDP. This year central banks are likely to have pumped in around 14 per cent of global GDP.

Finally, and maybe most crucially, governments implemented austerity in the years after the credit crisis in an effort to get their budgets back into balance as quickly as possible. This time, deficits have blown out massively and governments have shown no indication that they intend to claw back their generosity for a long time yet. Then, investors need to factor in that the US Federal Reserve this summer altered its monetary policy framework to put unemployment and social fairness front and centre and said it would be much more willing to allow inflation to run hot if in earlier parts of the economic cycle it was too low.

So whereas monetary and fiscal policy were pulling in opposite directions 10 years ago, this time they’re working in tandem. As long as social distancing is in place and economic activity is continually interrupted by lockdowns, all this stimulus is only ever likely to mitigate the consequent fall in demand.

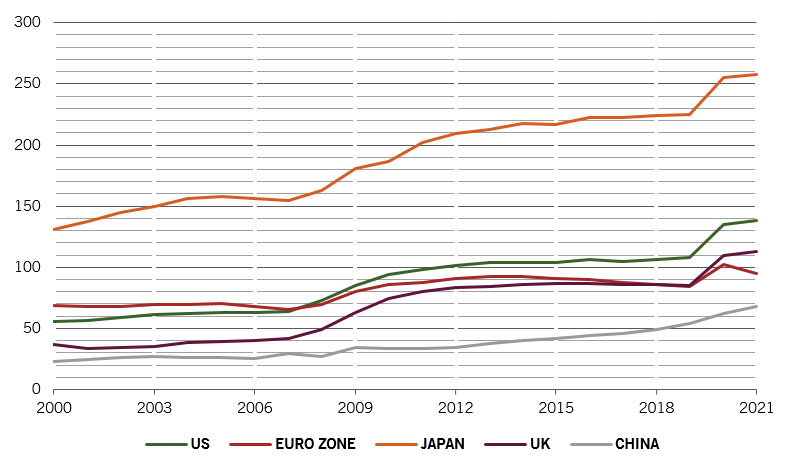

Fig. 1 - But is it sustainable?

National debt to GDP ratios, % of GDP, Pictet Asset Management forecasts for 2020 and 2021

But as soon as there’s a return to normal social interaction, as soon as people go back to travelling, eating out, going to theatres, shops and work as they once did, then these huge infusions of both fiscal and monetary stimulus will start to feed through to the prices of goods and services – and possibly faster than many people think.

Longer-term, all this stimulus also raises risks for social stability. Central banks’ approach to monetary policy has already created disharmony by favouring capital over labour. This disharmony is likely to have profound consequences for bond investors.

In a nutshell, the Phillips Curve – which describes the inverse relationship between unemployment and inflation – is a function of the relative pricing powers of capital and labour. Normally, the more demand there is for labour, the greater workers' pricing power, the faster that wages rise and thereafter inflation. But QE has effectively made capital free for corporations, giving them near-infinite pricing power, in effect taking that it even further away from labour. Because it’s free, capital has been misallocated. At the same time, unemployment can be driven down without giving labour bargaining power over wages. Stock options for management, share buybacks, a lack of productive investment all stack the economy against workers. Those imbalances will be made worse if inflation starts to rise faster than wages.

But that's a long-term issue, right?

We’ve already started to see its effects. As they’ve come to resent their lack of economic power, workers have started to look for other solutions, solutions that generally aren’t very business friendly. The rise of populism, tariffs, and violent demonstrations are part of this trend. This will cause even more market volatility than we have seen during the past decade, not just in equities, but in also in bonds.

Central banks’ efforts to mitigate the effects of market fluctuations has just made things worse. This interventionism makes investors complacent, encouraging them to chase returns, driving asset prices ever higher, to where they’re no longer supported by fundamentals. Then something happens to make investors reconsider their optimism, causing them to flee the market, at which point central banks have to step in again.

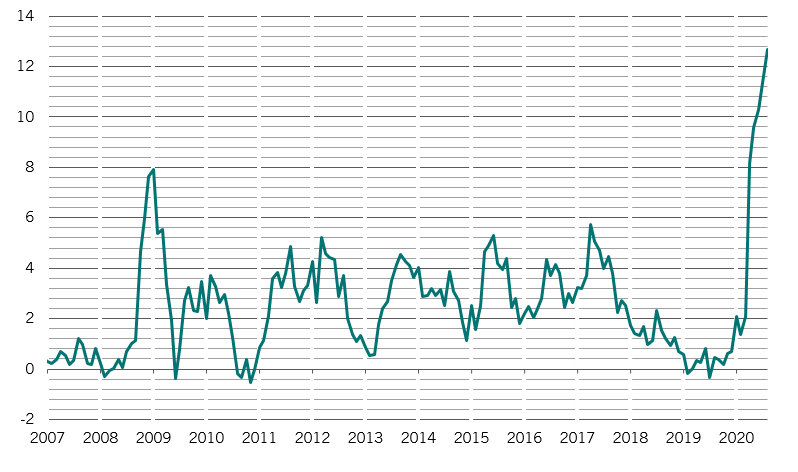

Fig. 2 - Awash

Policy liquidity for US, China, EMU, UK and Japan central banks, 6 month rolling % of GDP*

In the bond market during the past decade, these cycles have occurred every 18 months to two years. We first had the global financial crisis in 2008 followed by the euro zone’s sovereign debt crisis a few years later. Then came the taper tantrum, the energy crisis of 2016, Trumpflation and then Covid. I’m not smart enough to tell you what the next trigger will be, but I know that there will be something, because investor psychology continues to follow the same pattern.

For instance, towards the end of last year we’d become increasingly concerned at how richly credit markets were being priced. We couldn’t have predicted Covid, but we knew that something would come up to make investors question their view of future. As soon as the scale of the pandemic became evident, investors panicked and there was wholesale flight from most asset classes. Large parts of the credit market went from being irrationally expensive to unduly cheap.

Once again, central banks threw investors a lifeline and once again they started pulling themselves up. Before long, they’ll have gone too far. Eventually, they’ll be like the cartoon character climbing a rope that’s not held up by anything. They’ll reach the frayed end, look round in panic and suddenly go wooshing down.

You can already see mispricing in parts of the market. For instance, the MOVE index, which measures Treasury yield volatility, was near historic lows before the crisis. It spiked up during March and April but has since fallen back to pre-Covid lows, levels that don’t seem sustainable. If the Covid crisis worsens over the near term, there’s bound to be even further compression in Treasury yields. If a vaccine is introduced, yields will almost certainly head higher. In either case, volatility will go up.

If government bonds are no longer the safe haven they once were, what's the answer?

Then it becomes even more important to work with the cycle, to be sensibly and cautiously contrarian. It makes sense to look for value after there’s been a market panic – in other words when the credit markets deliver equity-type returns at bond-type risks. Of course you need good, penetrating analysis to avoid the value traps.

And then, when investor confidence gets ahead of itself, when credit starts to deliver bond-type returns for equity-type risk, then it’s important to rebalance and retrench until the next cycle hits.

People forget volatility can return very suddenly. As I said, these cycles are much more frequent than investors seem to recognize.

A traditional portfolio constructed of 60 per cent equities and 40 per cent bonds no longer makes sense.

In between, there are sweet spots for investors – periods of market dislocation and significant yield dispersion – like we have now. Some assets become overpriced as they draw strong flows, others are forgotten and still offer value. Though here it’s important to retain sufficient liquidity – which also means being aware that liquidity hedges which seem to work in the good times might not in times of market stress.

Unconstrained investors can roam the markets to find sources of value. Of course, they have to be nimble and have to have clear insights into what’s driving a particular asset as well as the market as a whole. But get this right and they can help to give investors what government bonds no longer can. Which is a reasonable, steady return, with controlled downside and as little correlation to equity like risk as possible.

related articles

Europe's defining moment

The EU pandemic recovery fund is a landmark deal that could transform Europe's economic prospects and revitalise its bonds, currency and stocks.

July 2020

Covid and the spectre of stagflation

Will huge amounts of stimulus trigger the sort of stagflation that ravaged the world in the 1970s? We don't think so.

June 2020

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.