[1] Wind, Standard Chartered Research as of 31.12.2020

[2] eVestment/Reuters

[3] Bond Connect as of 31.12.2020

[4] Roland Berger, on mutual fund assets under management basis

[5] Yield in local currency as of 07.04.2021. Source: Bloomberg

[6] All indices are total return and in USD unless indicated. Based on monthly data from 31.10. 2008 – 31.12. 2020. Source: Chinabond, JP Morgan, HSBC, Bloomberg

[7] Source: Chinabond, JP Morgan. All indices are total return and in USD. Based on the following periods: Great Financial Crisis (Aug-Oct-2008); EU sovereign debt crisis (Aug-Nov 2011); Covid-19 (21.02.2020-15.04.2020)

[8] Bloomberg Barclays China Composite index, USD unhedged basis, global agg and USD IG Source: Bloomberg Barclays

[9] IMF: The Future of China’s Bond Market, March 2019

Select your investor profile:

This content is only for the selected type of investor.

Investisseurs particuliers?

China's renminbi debt: a new line of defence?

Why Chinese onshore bonds are becoming an indispensable asset class for international investors.

Written by

Cary Yeung

Head of Greater China Debt

Just over a year after the Covid-19 outbreak began causing economic turmoil around the world, it appears investors may have discovered a new defensive asset: Chinese renminbi debt.

The USD16 trillion bond market has come through the crisis exhibiting the sort of stability normally associated with benchmark US Treasuries.

Not only did it hold up better than developed market government bonds during a tumultuous first quarter of 2020, it has also since traded within much narrower ranges. Its potential as a risk mitigation tool has also been thrown into sharp relief.

Over the past several months, renminbi bonds have not moved in lockstep with the world's other major bond markets. Neither have they tracked emerging market assets. All of which suggests they could turn out to be a good hedge against the riskier assets investors hold in their portfolios.

One explanation for this new-found resilience is that reforms in China have allowed renminbi-denominated bonds to feature more prominently in mainstream global bond benchmarks.

In March, FTSE Russell announced Chinese government bonds will be included in its flagship benchmark indices. That came on the heels of similar moves by JP Morgan and Bloomberg-Barclays.

Index inclusions are landmark developments, both for China and for investors worldwide.

For authorities in Beijing, they are a stamp of approval for their efforts to liberalise the country's capital market and integrate more fully into the international financial system.

For investors, it opens up a new world – one where the renminbi becomes a genuinely global investment currency. In other words, China's onshore bond market will play a far greater role in international bond portfolios.

China's USD16 trillion onshore bond market will play a far greater role in bond portfolios.

Foreign ownership of Chinese bonds was already rising in anticipation of the index changes.

Non-Chinese investors built up their holdings of RMB debt to RMB3.2 trillion by December 2020, up nearly 50 per cent from the same month a year before.1

Of the USD9.5 trillion of assets under management from corporate and public pension funds globally, 0.26 per cent was held in Chinese bonds as of the third quarter of 2020, up from 0.04 per cent in 2015.2

Further boosting the market's international standing, China has delivered a series of reforms to make it easier for foreigners to access the market.

Among the most important, the “Bond Connect” programme, launched in 2017, allows non-Chinese investors to trade in Hong Kong without an onshore account. Already, 75 out of the world’s top 100 asset managers have joined the programme while trading volume doubled last year to RMB4.8 trillion.3

All of which means the inflows seen since the pandemic are likely to be part of a much larger reallocation. According to the International Monetary Fund, index inclusion alone could result in capital inflows of as much as RMB7.4 trillion into Chinese bonds from international investors.

Opportunities beyond pandemic

Policymakers are also keen to attract foreign funds to hasten the development of the asset management industry across the country.

This is a priority for Beijing as the country’s rapidly aging population demands a sustainable pension system.

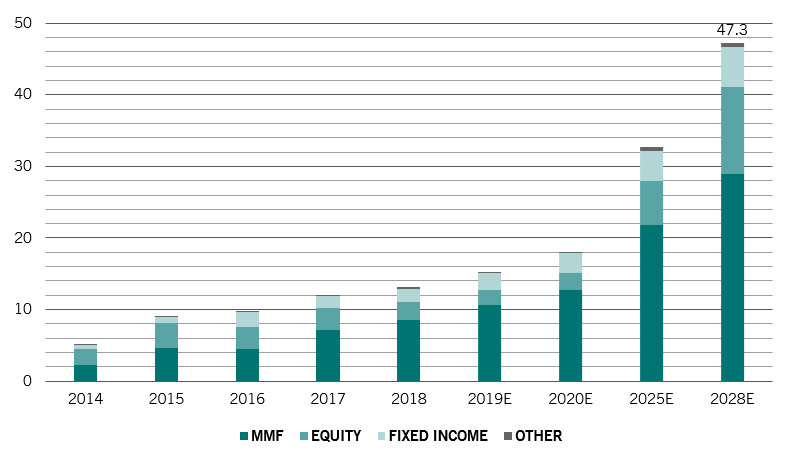

China’s asset management industry – fund houses, insurers and securities and trust companies – is expected to triple in the 10 years to 2028 to RMB47.3 trillion as Beijing removed all foreign ownership restrictions in April 2020.4

This should help diversify the domestic and foreign institutional investor base for Chinese securities, which is currently dominated by commercial banks.

Foreign investors make up just under 3 per cent of total holdings today, which we expect to rise to 3.3 per cent this year.

Home-grown industry

AUM growth of China's asset management industry by asset class, RMB trillion

Calm amid turmoil

The opening up of the market comes at a time when the fundamentals of Chinese local currency bonds look particularly strong.

Yields offered by onshore RMB bonds are attractive to international investors as a record USD16 trillion of global bonds yield below zero.

The five-year Chinese government bond yield stands at 2.9 per cent, compared with 0.9 per cent for US Treasuries, -0.1 percent for Japanese Government Bonds and -0.7 per cent for German Bunds with the same maturity – differentials that have never seen before.5

Yield is not the only selling point. They also offer a means of diversification. Chinese bonds's returns do not correlate especially strongly with those of any major global asset class – bond or equity.

The correlation of returns from renminbi bonds with those of US and European government debt and equities, for example, is less than 0.2.6

What is more, Chinese bonds have exhibited remarkable resilience during historically volatile periods, such as the 2008 global financial crisis and the European debt crisis.

The Covid pandemic was no exception. Renminbi bonds were among the few asset classes to deliver positive returns during the sharp sell-off of the first quarter of 2020, performing more in line with other G10 government bonds.7 Of greater significance was that their maximum drawdown for 2020 - their peak-to-trough decline - was just 2.2 per cent, a fraction of the losses endured by global bonds (around 9 per cent) and US dollar investment grade credit (over 15 per cent).8

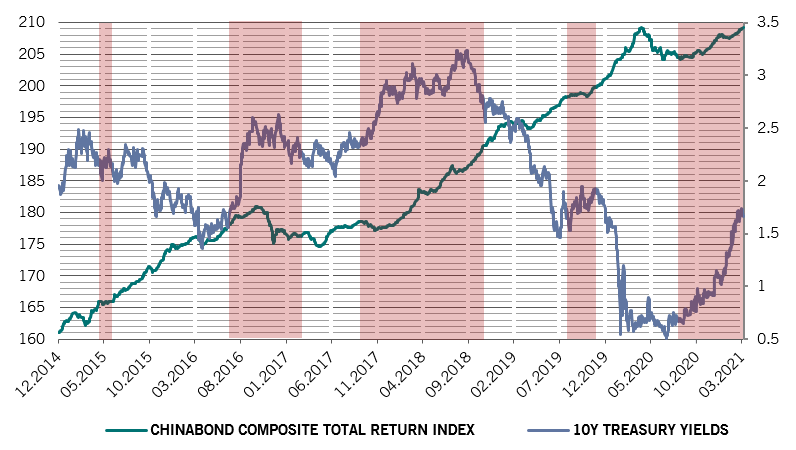

Chinese local currency bonds have also proved to be historically resilient to rising US yields. In the most recent global bond market sell-off, they have performed better than any other fixed income asset classes (see chart). This further reinforces their standing as a defensive asset.

Resilience

Chinese local currency debt has remained resilient in times of rising Treasury yields (RHS, %)

RMB - an international currency

As the world’s second largest economy matures, Beijing is committed to opening up its financial market and promoting the greater use of the Chinese currency abroad.

The authority has already established the CIPS, a payment system which offers clearing and settlement services for its participants in cross border RMB payments and trade, and opened commodity futures contracts in the RMB.

China’s drive to internationalise the RMB also includes some innovative projects. For example, the People’s Bank of China issued digital currency in October to 50,000 randomly selected consumers in what is its first public test of the digital payment system.

Pilot schemes like this should also help encourage users in other countries to use the RMB. The RMB is already the world’s fifth largest reserve currency but it accounts for just under 2 per cent of the total central bank reserves.

If that share were to double, it would amount to an additional RMB1.5 trillion of RMB bond investments, the IMF says.9

According to Pictet Asset Management's economists, it won’t be long before the RMB’s share of international reserves is greater than that of the British pound.

All of this is likely to lead to a greater appreciation of the RMB, which should contribute strongly to the total return of investors’ bond portfolios.

Going green

Another favourable development is China’s recent announcement that it plans to be carbon neutral by 2060.

The ambitious goal is likely to require as much as USD16 trillion of investments, where we believe green bonds will be an important channel.

The PBOC has already promised to improve the country’s green finance standards to support the 2060 goal and make it easier for foreign investors to enter the green finance market.

As of June 2020, China’s outstanding green bonds totalled RMB1.2 trillion, the second largest in the world.

This figure should grow in the coming years, helping expand the universe and increase the depth of the Chinese onshore bond market in the long term.

RMB-denominated bonds should become an even more integral part of global fixed income investors’ portfolio.

With its population ageing rapidly and its investment needs rising as a consequence, China has every incentive to remove restrictions on the flow of capital across its borders and drawing in foreign funds.

And nowhere other than the RMB onshore bond market can investors see China’s economic transformation more clearly in the coming years.

As the year of the Ox promises to bring growth for Chinese RMB-denominated bonds, the asset class should become an even more integral part of global fixed income investors’ portfolio.

more on china and asia

New Asian century: post-pandemic opportunity

Why emerging Asian assets will grab a greater share of global investors' portfolios.

February 2021

Onshore vs. offshore China bonds

“China Bonds under the Radar” series aim to provide insights into the 2nd largest bond market in the world - China onshore bond market. In this month’s piece, we provide a brief comparison of China’s onshore and offshore bonds markets, and discuss the differences and connections between the two.

February 2021

Important legal information

The Pre-Contractual Templates (PCT) when applicable, the Key Information Document (KID), as well as the Prospectus must be read before any decision to invest. The Prospectus (in English and in French), the PCT when applicable, the KID (in French and in Dutch), as well as the latest annual and semi-annual reports (in English and French) are available free of charge at our financial Belgian agent CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles or at the management company, Pictet Asset Management (Europe) SA, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, as well as in digital format at www.assetmanagement.pictet.

The summary of investors rights is available here and in French and in Dutch at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The NAV are available at www.beama.be.

Claims and Mediation Service: For any claim you can contact Pictet Asset Management (Europe) S.A., Compliance Department, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg or the Consumer Mediation Service (Service de Médiation pour le Consommateur), North Gate II, Boulevard du Roi Albert II 8 in 1000 Bruxelles or at www.mediationconsommateur.be. The Mediation Service may suggest solutions for the settlement of the dispute. In the absence of agreement on the proposed solutions, each party may bring proceedings before the competent courts.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future.

Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

This marketing material is not intended to be a substitute for the fund’s full documentation or any information which investors should obtain from their financial intermediaries acting in relation to their investment in the fund or funds mentioned in this document.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.