[1] Ranking based on 1) Quarantine efficiency, 2) Government efficiency of risk management, 3) Monitoring and decisions, 4) Healthcare readiness, 5) Regional resilience, 6) Emergency preparedness. Source: Deep Knowledge Group, Pictet Asset Management

[2] Source: Refinitiv and Pictet Asset Management

[3] Households spending USD11-110 per day per person in 2011 adjusted for purchasing power parity. Source: Brookings Institute

[4] Source: Goldman Sachs and MSCI

Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

New Asian century: post-pandemic opportunity

Why emerging Asian assets will grab a greater share of global investors' portfolios.

Written by

Patrick Zweifel

Chief Economist

Luca Paolini

Chief Strategist

A year after the Covid-19 outbreak triggered widespread social and economic upheaval, Asia is emerging out of the crisis stronger and with greater influence on the world stage, pulling the globe’s economic centre of gravity steadily to the East.

Economic activity across the region has largely returned to where it was before Covid-19 struck, thanks to its exemplary management of the pandemic. (Asia’s Covid safety and resilience are ranked as the best in the world.)1

What’s more, the bloc’s anti-crisis economic policies have been prudent and measured, in contrast to the West, where governments and central banks have been forced onto a war footing.

Take China. Although it was at the epicentre of the pandemic, policymakers there have not had to resort to excessive fiscal or monetary largesse. China has not experienced a build-up in borrowing on the scale that developed economies did. The world’s second largest economy went into the crisis with public debt at below 50 per cent of GDP, which we forecast to rise to 67.7 per cent by 2022. The picture is similar in the rest of emerging Asia, comparing favourably with G5 economies where the average debt-to-GDP ratio should exceed 150 per cent by 2022.2

In other words, Asia has managed to support growth without sowing the seeds for future financial risks.

We expect the bloc’s GDP growth to rebound strongly to 8.9 per cent in 2021, ahead of advanced economies which should grow just 4.9 per cent. That performance looks stronger still when set against the region’s shallow contraction of just 0.2 per cent last year, compared with 5.2 per cent for its developed counterparts.

Asia has managed to support growth without sowing the seeds for future financial risks.

Asia’s effective handling of the pandemic and its economic resilience owe a lot to a series of path-breaking structural reforms which the region has been advancing in the past 20 years or so, a process which we expect will pick up pace the coming decade.

Since the currency crisis in the late 1990s, Asian nations have strengthened the foundations for long-term prosperity by reforming their institutional, regulatory and capital market framework and boosting international competitiveness.

Deeper regional integration is another linchpin of post-pandemic economic revival. In November, EM Asia unveiled a new ambitious trading pact – the Regional Comprehensive Economic Partnership agreement (RCEP) – which covers trade in goods, services and investment among 15 countries, home to 30 per cent of world population.

The deal should help boost long-term growth even more by lowering trade barriers and further lifting foreign direct investment. Asia’s FDI remains resilient despite the pandemic. In 2020, China beat the US as the largest recipient of FDI in the world, attracting USD163 billion.

Southeast Asian countries, such as Vietnam, less developed than its Northern counterparts, should benefit the most from the new pact as they build a manufacturing base that will capitalise on demand from importers keen to diversify away from China.

Vietnam is one of the most dynamic Asian nations, offering high political stability, a deeply integrated global market and abundant labour with its young population of 100 million people. Its successful handling of the pandemic has added to the country’s credentials. Thanks to its geostrategic connectivity to China and the rest of Asia, Vietnam should attract a greater share of FDI in the coming years.

At a pan-regional level, Asia’s living standards are improving fast and its population is becoming more urban and affluent. By the end of the next decade, Asia will account for two thirds of the planet’s middle-class3 – a cohort whose consumption and investment habits will transform the business landscape.

Post-pandemic powerhouse

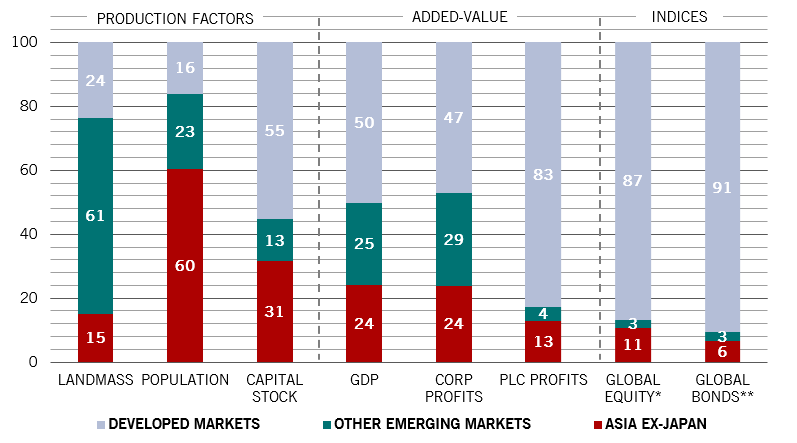

Asia’s rise will have far-reaching implications for investors. Not least because the financial markets have yet to take notice. A glance at the world’s equity and bond indices shows Asia is woefully under-represented.

Emerging Asia makes up a mere 10 per cent of the global equity market index and just 3 per cent of the bond counterpart – even though it accounts for around 24 per cent of both the world economy and global corporate profits (see Fig. 1).

Fig. 1 - Under-represented

Economic fundamentals compared with equity and bonds indices, % weight by region

That disparity will not remain for much longer. As the region’s capital markets gain depth and open up to foreign investors, Asia is certain to become a much bigger feature of the investment universe.

Unsurprisingly, China is the disruptor in chief. With its population ageing rapidly and its investment needs rising as a consequence, the world’s second largest economy has every incentive to integrate more fully into the global financial system, drawing in foreign capital as it does so.

To achieve that, it needs to press ahead with reform. Here, the signs are encouraging.

Beijing has already relaxed rules to make it easier for foreign investors to trade Chinese bonds; it has also launched a new Nasdaq-style stock exchange and introduced other initiatives to attract funding into its burgeoning technology and artificial intelligence sectors.

The global health crisis is not slowing the pace of reform. To the contrary. In October, China detailed steps to grant more autonomy to Shenzhen, letting the southern financial and technology hub pilot reforms in market development and economic integration. Under the trial scheme, Shenzhen will launch stock index-futures and issue offshore yuan-denominated local government bonds, while some companies will be allowed to issue shares.

Responding to these changes, global index providers have started to incorporate more Chinese assets in their bond and equity benchmarks. It is a development that is expected to generate combined inflows of more than USD300 billion in the coming years.4

The near-term economic prognosis is also sound. We expect China’s GDP to grow 9.5 per cent in 2021. Another Asian power house India, which suffered a sharp contraction in 2020, should bounce back strongly in 2021 – we expect its economy to grow 13.1 per cent.

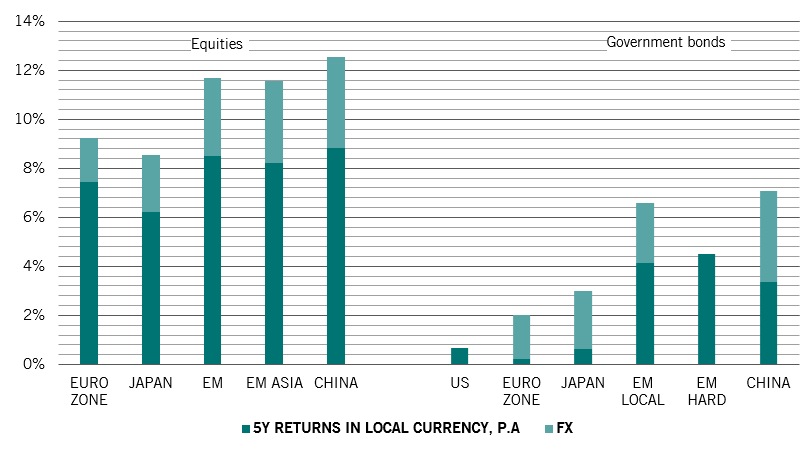

Asia’s superior growth profiles should also help boost the region’s asset performance over the next coming years. We expect emerging Asian stocks to gain nearly 12 per cent every year in the next half a decade – nearly double the pace of those in developed markets. Asia’s local currency debt should also perform strongly, notably in China, at a time when investors in developed market bonds face the prospect of capital losses once adjusted for inflation (see Fig. 2).

Fig. 2 - Asset class return forecast by region

It has been long predicted that if the 19th century belonged to Europe and the 20th century to the US, the 21st century belongs to Asia. The region is poised to grab a greater slice of international investment as it develops into a strategic asset class. Investors will have to change their portfolio allocations to reflect Asia’s growing heft.

Related articles

Why invest in Asia? An opportunity investors can no longer ignore

What international investors can learn from China's pandemic recovery

September 2020

Chinese onshore bonds: going mainstream

The inclusion of renminbi-denominated debt in the flagship global benchmark bond index will transform the asset class into a strategic investment.

February 2020

A class apart: emerging Asia's fixed income market

Why investors seeking a stable and attractive source of return within a diversified bond portfolio should head to emerging Asia.

December 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.